Whatever it takes…

For many, 2020 will go down in history as annus horribilis, but this do not apply to the financial markets. During the year, the central bank governors have repeated Mario Draghi’s formula from 2012 several times to convince the market. But words alone are not enough.

For many, 2020 will go down in history as annus horribilis, but this do not apply to the financial markets. During the year, the central bank governors have repeated Mario Draghi’s formula from 2012 several times to convince the market. But words alone are not enough.

The chart above is from the Economist on March 24, 2020 where they argue that the words do not bite this time when Covid-19 has caused most countries in the world to shut down.

Source: McKinsey & Company

But after that, the central banks also opened their taps. The graph above shows the support this year in light blue, compared with the support after the financial crisis. For many countries such as Germany, Japan, France and the UK, the support has increased by a factor 10. In the United States, which stood on the barricades during the financial crisis, support is lower than in the European Union and Japan. But this is largely due to support stuck in the US Congress when Democrats and Republicans do not agree. As soon as a new president is appointed in the United States, the support is expected to come, but the longer the wait, the more negative the effect on the economy, of course. Note that China is missing in the summary above. Our assessment is that they probably have stimulated more than any other economy, but that this is not visible in the statistics.

Pending support in the US, the Fed chief has reassured the market with unreserved support:

“The Fed will stay here and be strongly committed to use all our tools to support recovery for as long as it takes until the job is well and truly done”.

So, is it all over?

It is impossible to say. However, the markets have learned that there always seem to be new stimuli after each crisis. Our thesis is that this can continue if there is confidence in the political system and in the central banks. Even though there are more and more riots around the world, it looks as if it is plenty of trust capital left for the central banks. The decade 2020-2030, however, is likely to be a shaky decade. It is easy to be friends in success. However, the world is going from a fantastic era when China became the whole world’s factory and increased the standard of living globally via increased productivity, to a world where China is increasingly being pushed into a corner and also moving towards a more strict internal atmosphere.

Covid-19 holds back the riots in the world by the simple fact that the participants in the protest movements are allowed to stay at home.With rising unemployment, renewed climated debate and Covid-19 in decline, the summer of 2021 has every opportunity to develop into a beacon in world history. Do not forget that many of the world’s crisis, with the Greek crisis and the Arab spring as the best example, germinate in the spring to flare up during the hot summer months.

The sitting elite in the world, manifested by Davos, argues that the economy needs to be reformed, but really only talk about more bread for the people. Hence we do not expect other recipes from the elite than additional support, as long as this works.

But it is a long time to the summer.

The S&P500 index has reached previous highs (but has 3645.99 intraday left to break). More important is the rising trend line, serving as a resistance. MACD is still rising and so is EMA9. The question is if the index has enough energy to break above.

Even more important is the development for Nasdaq. Throughout the Covid-19 pandemic, tech stocks have performed strongly. Partly because tech was considered a protected sector and partly since investors have pushed a lot of money into the market. Somewhere all this money should be allocated. When vaccine candidates started to progress, tech stocks fell in favor of value stocks. In the two last weeks, the stocks that have performed the worst during the pandemic have turned and performed best. Now you see how the interest in tech stocks have returned when Nasdaq is about to be able to break up again.

Apple stocks refuses to break out of a wedge formation. The more time that passes, the more energy accumulates. Technically, this formation has great opportunities to break out in the direction of the trend, i.e. upwards.

But one should also not forget the context. As shown in the monthly graph below, Apple has risen parabolically during the Covid crisis. This rise collapsed during September-October.

The Tesla share is getting close to the 600 USD-level and the formation calls for further upside:

The graph below shows how growth stocks (tech) took some revenge last week on the value stocks that have otherwise been winners since the first vaccines showed positive result. The bottom line is how the correlation begins to increase between the types of shares. The computers have now been rigged to trade between these types of assets. From a defensive investor perspective, it may well be worthwhile to study equities with high direct returns for 2021.

The index composition of OMXS30 is favored by this rotation as well as by the weaker SEK. OMXS30 opened weak on Friday but managed to close 0,3% up. A rising EMA9 serves as a support but as shown, MACD-histogram is falling implying that the positive momentum is losing speed. In case of a break below EMA9 – the next level can be found around 1 905:

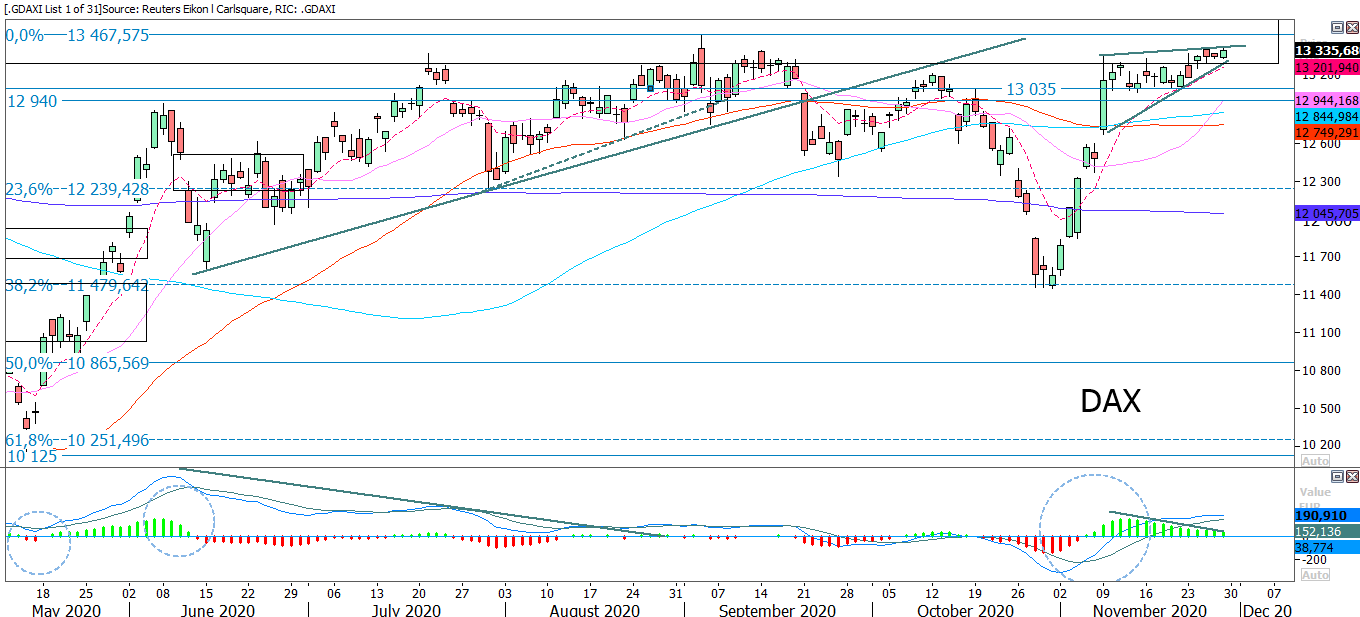

The German DAX index has now penetrated the old gap for several days. One might think that the massive subsidies in Germany will bear fruit one day. However, one should not forget or underestimate that Germany’s important export markets are in a lockdown.

Note how DAX is trading in a bearish rising wedge as MACD histogram is falling. This is typically a setup for a downward movement. The 13 035-level and MA20 serves as first and second support levels in such a scenario.

Bitcoin managed to break back up above EMA9 and MA20. The question is if the previous top from November can be reached:

Raw materials are, just as we wrote last week, hot. The copper price breaks up again and Brent oil closed last week above Fibonacci 50 as well as MA50. Note also how MACD has generated a buy-signal. See the weekly graph below. The next level on the upside can be found around 50 USD/barrel:

One reason why the DAX index is being held back can be seen in the EUR/USD graph below. The euro is lifting against other currencies in the ugly contest that is taking place between all the world’s currencies. Note the break above the resistance. Should the 1.2-level be tested again? It is at 1.2 against the USD and is said to be an absolute limit for how much stronger the ECB can withstand against the USD. If this is true, the ECB will act in some way- either by selling EUR and buying USD, which will take place either in disguise, with vocal statements or a combination of both. Also note how the currency pair is trading in a bearish rising wedge:

In the general euphoria over the vaccines, the gold price continues to be beaten. It may be time to start picking gold soon, but there are no buy signals yet so the risk aversive might wait. Note how the gold price closed below MA200 and that Fibonacci 50 is meeting up:

Risks

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.