The stock market behaves like an unstable fighter jet

Rising prices remain a concern. If you google this phenomenon, you will learn that this applies from everything from copper to corn, barley, mustard seeds from India to wages. The world economy is in the aftermath of a giant external shock that the models probably cannot handle. The central banks have also taken on the task of dealing with this turbulent economy through more active measures directly in the market. We doubt that the central banks would be better than Adam Smith’s invisible hand in governing economies.

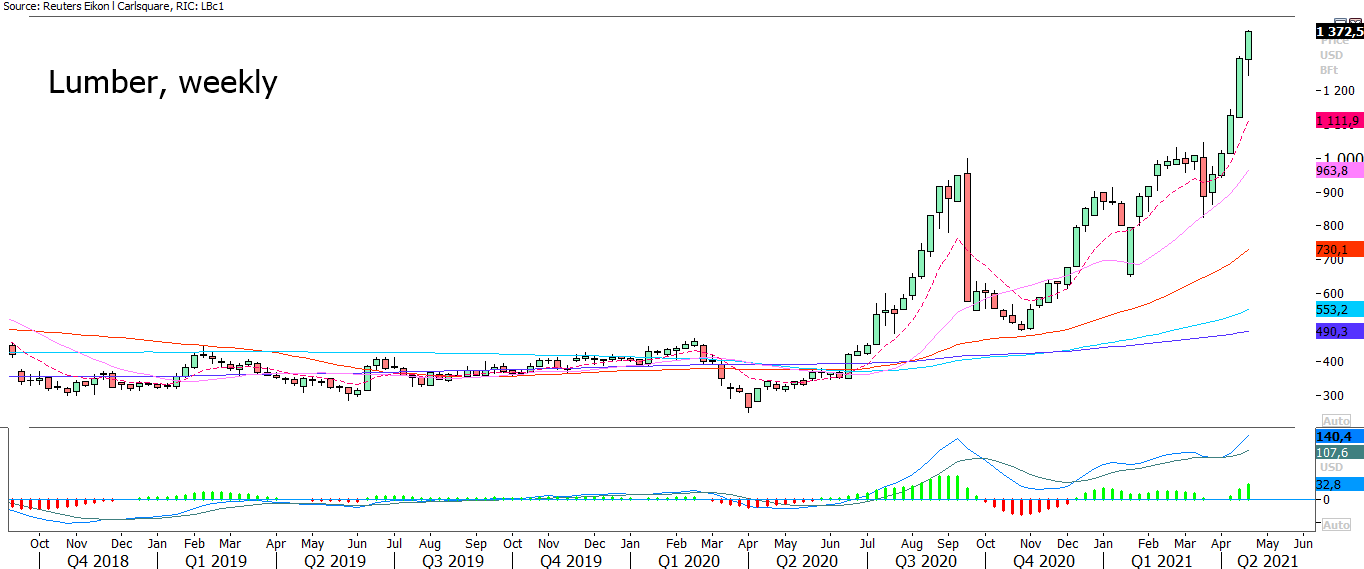

Rising prices remain a concern. If you google this phenomenon, you will learn that this applies from everything from copper to corn, barley, mustard seeds from India to wages. What is quoted right now in the blogosphere are the prices of lumber or timber:

It goes without saying that if timber prices rise, this will have an impact on the construction industry in the form of higher construction costs. Where possible, this will be passed on to the next link in the value chain, which will be construction companies, project companies, property owners and ultimate tenant-owners. According to an article in the London Free Press, prices have more than doubled in the past year, before and after Covid-19, which is also reflected in the graph above. There is a particular shortage of plywood and other construction materials. This is partly due to a lack of freight capacity and the fact that many sawmills have reduced their production, but also to pests in the forests. Demand for houses remains high, which drives up prices. The construction cost of an average house has thus risen by USD 35,000 in the past year in the United States.

Shipping freight rates have also risen dramatically. There is a mountain of goods to be transported when the countries wake up from their Covid-19 hibernation. This means that the immediate supply of freight capacity is low. However, we estimate that this is a temporary phenomenon. This is since we believe that the global supply of vessels is large enough to saturate demand in the longer term. The latter is the recurring theme in the central banks analyzes. The effects are seen as transient. Before we delve into this issue, let us give a few more examples:

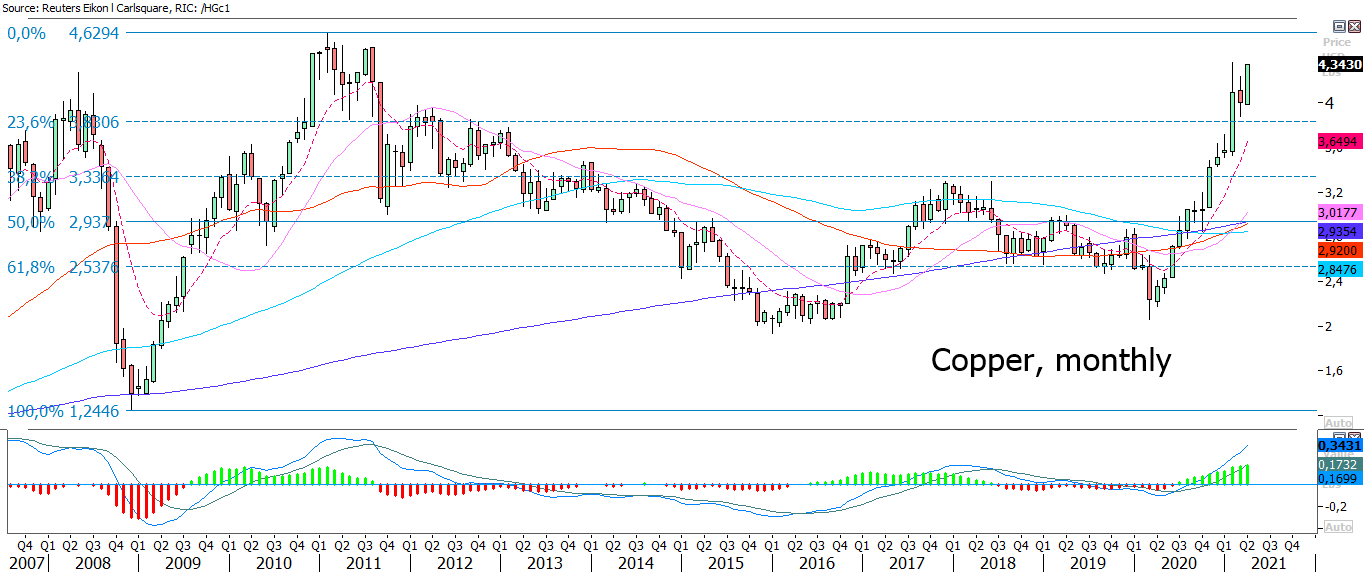

The copper price is on its way back to All-Time-High.

DBA is an ETF that reflects to price of agricultural products. After a long slippery landing, the price has broken up:

An important component of DBA is corn. There is a real fire under this commodity now. But this applies to all agricultural products. It becomes very noticeable for those who read the local press as from India about the price of mustard seeds:

Below is the future for corn:

Rising prices remain a concern. This is because rising prices are the same as inflation. Prices for construction products such as timber have doubled.

In the Atlanta Fed’s price model for goods that are rapid in its price changes, you can now see how inflation increased by 21 percent in March and by 6.3 percent compared with a year ago.

So far, we have talked about the price development. Another component of inflation is wages. The graph above should give all central bank governors a scare. It shows how wages have risen by 4.4 percent, which should give rise to a real inflation fire. But really, the graph shows a different picture. Note that wages have circulated around zero and that it is only in the last year that wages have risen. The reality we see on the stock market screens with ever-rising share prices is not reflected in the labor market. People have not gotten better. With ever-rising house prices, which are poorly reflected in inflation measures, people have probably rather gotten worse in recent decades. This reflects developments in the United States, but we do not believe that there is a huge difference from developments in Europe. In other words, the gaps between rich and poor continues to rise.

In view of the sharp rise in recent months, it is unfortunately heading in the same direction. It is not the wages that have risen- it is the base that has changed. Covid-19 has deleted many low-wage jobs in the service industry, which has meant that these jobs have fallen out of the statistics. This gives high-wage jobs a larger share of the pie, which gives the optical illusion that wages have risen overall.

If you start to investigate this, the picture becomes extremely complicated.

The real interest rate remains around zero, which reflects that the fixed income market does not discount any rapid increase in inflation. However, we suspect that this picture is manipulated by central banks that buy bonds to calm the market.

Everything must be weighted together in an extremely complicated analysis. We doubt that even the central banks have models that come close to reflecting the underlying driving forces that exist in the economy. They may be able to cope with a normally developed business cycle. But right now, the world economy is in the aftermath of a giant external shock that the models probably cannot handle. The central banks have also taken on the task of dealing with this turbulent economy through more active measures directly in the market. We doubt that the central banks would be better than Adam Smith’s invisible hand in governing economies.

With all the support, the economy risks functioning as a modern fighter aircraft like the JAS 39 Gripen. To get the maximum maneuverability, the plane is deliberately built as unstable. Instead of the pilot handling the flight with manual hand grips, it is a computer that interprets all the pilot’s hand grips and performs the maneuvers. That is possible for as long as possible, i.e., until the computer calculates incorrectly due to wrong input data or when the computer cannot longer handle all the data. If this happens, it will probably be more than one central bank governor who shoots himself or herself out of the plane before the crash.

In any case, the Fed has managed to get a nice slippery slope of the 10-year US government bond after a few weeks of inflationary turmoil.

We believe, just like the central banks, that the soaring prices in the underlying economy will be temporary. Unlike them, however, we raise a warning finger that this can create volatility in the markets and, in the worst case, trigger a mini crash if panic takes hold in the herd. But this market cannot be handled with fear as a guiding measure. Instead, one must continue to trust that the central banks will continue to squeeze money into the system and that this will benefit the stock market. Furthermore, we must assume that the central banks will handle new volatility with additional support. This is a recipe that will work if there is trust capital for the central banks. So far, it is the most insignificant actors like us who criticize the prevailing policy, which does not make much difference to the general view of the market.

For the equity investor, there are two options. Either be a very long-time saver who chooses companies with secure cash flows and completely ignores the turbulence in the stock market. Alternatively, you can be an active player who decides to step on and off in line with the development.

For those who want to delve deeper into the central bank issue, we recommend an article from Catella who warns that banks can reduce their loans if the central bank support policy continues. The reasoning is interesting, and the phenomenon has been addressed earlier when the central banks complained to the ordinary banks that they did not lend funds. We do not know, but possibly this is a partial explanation for the explosion of corporate bonds we are now seeing, which is a way to bypass the banks and borrow directly in the capital market:

www.fastighetsvarlden.se/notiser/catella-uppmarksammar-marklig-finansieringseffekt/

The Q1 2021 reporting season

Sandvik’s Q1 2021 report was roughly in line with markets expectations. Order intake increased by 12 percent organically at Group level, but the majority of this disappeared with currency translation effects. As for the sectors, Sandvik sees a positive trend for mining and vehicles, flat for engineering and civil construction and a negative trend for energy and aviation. In terms of regions, the increase figures for order intake were very strong (26-38 percent) in Asia, Africa, and Australia. However, the increase remained at 1 percent in Europe and 5 percent in North America. The comparative figures for the latter regions will be easier to surpass in Q2 2021. In terms of pretax profit, however, Sandvik’s earnings in Q1 2021 ended up at only about 60 percent of the level from Q1 2020.

Volvo surprised the stock market with a super strong Q1 2021 result (23 percent better than expected at EBIT level) and an order intake for trucks that exceeded forecasts by about 40 percent. The increase is primarily attributable to China and India and to some extent to Brazil. Volvo raises the full-year forecasts for the truck market in China by 130,000 trucks (plus 9 percent).

SKF, whose Q1 2021 report turned out worse than anticipated, still confirms the above view of activity and demand in the industry. The company puts several pluses in most customer segments in the Asia-Pacific region. It also looks positive for trucks, the vehicle aftermarket, energy systems and industrial distribution in Latin America. Other positive sectors are trucks, the vehicle aftermarket, electric industry and industrial distribution in Europe, the Middle East and Africa.

For the banks, the reversion of anticipated credit losses plays a significant role in the banks’ positive earnings outcome in Q1 2021, both in the US and Sweden.

When 123 of 504 S&P500 companies (i.e., about 25 percent) have reported their Q1 2021 results, the proportion that surprised positively is still high (85 percent). At the same time, the proportion who managed to exceed the revenue forecasts has decreased to 77 percent. Apart from US domestic sectors such as utilities and real estate, it is the industrial sector and non-cyclical consumer goods companies that have managed to surprise relative least positively. IT/Technology is at most 100 percent better than anticipated. This is even though 13 companies have reported so far. This is interesting since several of the leading large companies in the IT/Technology sector are to report their Q1 2021 figures this week.

Profit growth for the S&P500 companies looks set to break a record in Q1 2021 with a forecast so far of plus 30 percent. This is the highest profit growth since Q3 2010. Meanwhile, revenue growth is about 7 percent, which is the highest revenue growth since Q3 2018.

If we count the sum of profits for the 123 companies that have reported and weight how much analysts have revised their figures in next quarter, we land on a 4 percent increase for Q2 2021.

A ranking of profit growth per sector in the S&P500 index shows that the financial sector with large banks such as JP Morgan Chase, Wells Fargo and others leads large, followed by Consumer Discretionary and Materials. IT/Technology is below the average for the S&P500 index. The engineering sector is the weakest sector in terms of profit growth among the S&P500 sectors. It is not quite the same pattern as we see on the Stockholm Stock Exchange, where most major engineering companies have come up with strong Q1 2021 reports. One explanation may be that Swedish companies have a significantly larger share of their revenues to an Asia that is going strong, while an average S&P500 engineering company receives some 50 percent of its sales from North America.

However, the P/E ratio valuation of the S&P500 index continues to be about 30 percent higher than the five-year-average. As before, there is a significant central bank doping element in the high share prices and not just strong results from the companies.

Momentum

President Biden’s proposal for increased capital taxes in the US is said to be pushing the Bitcoin exchange rate. We have a challenging time believing that these proposals will go through the US Congress. This should in other words be a buying opportunity for Bitcoin. But the flows in Bitcoin are difficult to predict from a fundamental perspective. Therefore, the graphs are more interesting. Bitcoin is now traded at a support on MA100, but MACD has generated a sell signal.

Bull & Bear Certificates

The S&P 500 index is consolidating. Perhaps the reports from the FANG-companies coming up this week will help setting a direction:

The tech-heavy Nasdaq index is also consolidating:

The Apple stock is consolidating ahead of the report on Wednesday 28 April:

The Facebook share has fallen ahead of the report on Wednesday 28 April. It is currently trading at a support around the psychologically importen 300 USD-level:

On the other hand, the Google (Alphabet) share is consolidating around its all-time-high ahead of the report on Tuesday 27 April:

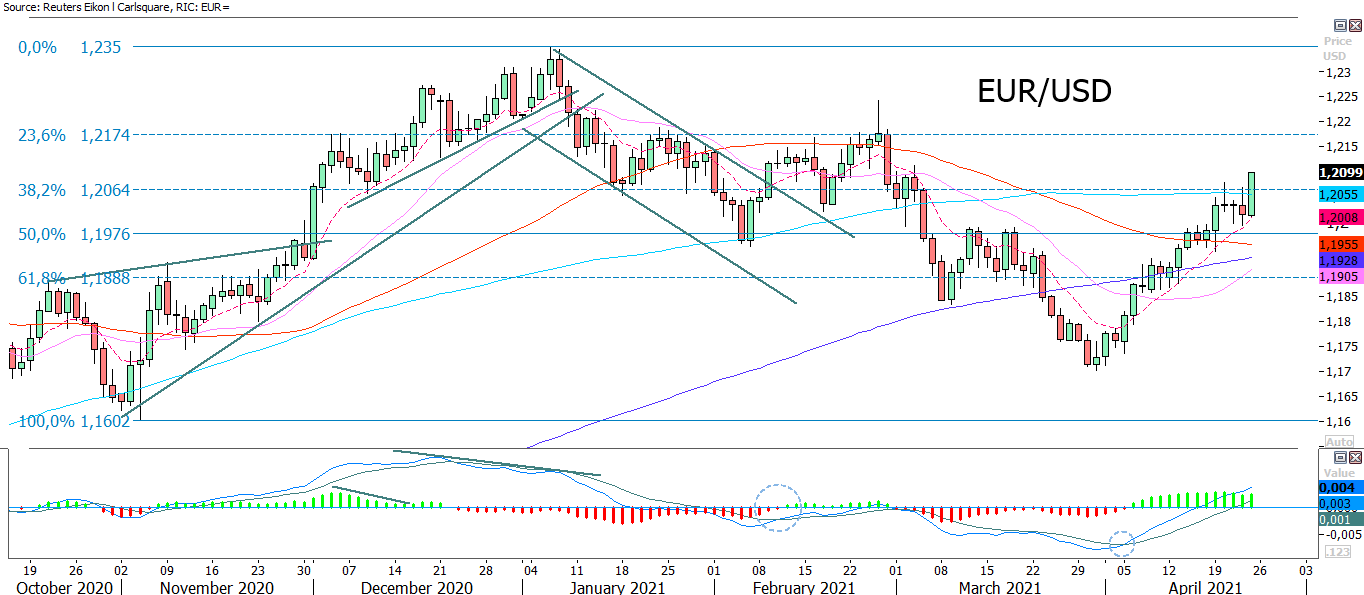

Interesting is that the EUR/USD closed at about a resistance in form of MA100 and Fibonacci 38.2 on Friday 23 April. A weaker USD helps driving prices up on assets quoted in USD. The next level on the upside for the currency pair can be found around 1.217:

In Sweden with the OMXS30 index, momentum is falling as can be seen by MACD. However, the index is still supported by MA20. In case of a break to the downside, the next level can be found around 2 150:

The pattern seems similar in the German DAX index. MA serves as a support on the downside, but in case of a break – the next level can be found around 14 800 followed by MA50 currently trading around 14 600:

Risks

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.