The IPO angle on current valuations

IPOs are booming. Global IPO activity, in terms of raised capital to September, has already exceeded the entire year of 2020. The year 2017 is still ahead in terms of the number of IPOs. 2018 was a volatile year that also caused the number of IPOs to fall.

In this weekly trading note from Carlsquare, we elaborate on the following topics, indices, and stocks:

- The IPO angle on current valuations

- High valuations a driver of IPO:s

- Are SPACs a forward-looking indicator?

- Higher inflation has had minimal impact on interest rates

- Momentum

- A nice finish in the US last week, but not very convincing

- Can Google set new highs under negative divergence?

- EUR/USD moves in line with the funding futures

- Gold is climbing in tandem – implying inflation may be here to stay

- Is OMXS30 ready to test the previous top?

- Volvo in good shape

- A new all-time-high for DAX

The IPO angle on current valuations

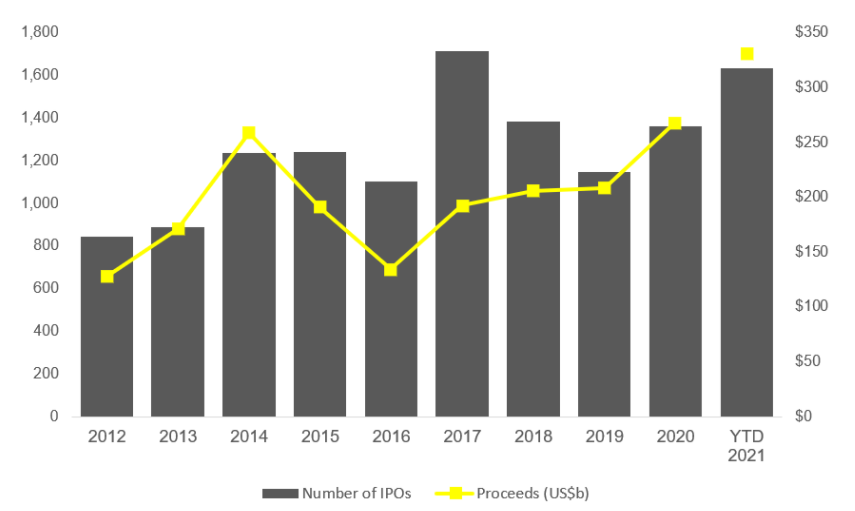

IPO: s are booming. Global IPO activity, in terms of raised capital to September, has already exceeded the entire year of 2020. See chart below. The year 2017 is still ahead in terms of the number of IPOs. 2018 was a volatile year that also caused the number of IPOs to fall.

2012-YTD (Jan-Sept) 2021 global IPO activity

Source: EY

2021 has been a record year for the US in the number of IPOs. However, in percentage terms, the increase of IPOs has been significantly higher in Europe, the Middle East, India, and Africa compared to the Americas so far in 2021, according to EY.

High valuations a driver of IPO:s

Over the past ten years, the value of S&P 500 companies has nearly quadrupled, up 290 percent or about 14.8 percent annualized value growth. Since January 1, 2020, the price increase has been about 23 percent per year. The link to this price appreciation and the increased IPO activity is apparent.

S&P500 index during the corresponding period from 2012 until YTD 2021

Source: Refinitiv Eikon and Carlsquare

There are many reasons for listing a company. The most obvious one may be the opportunity for the company to go to the public to raise new capital. It is also a way to get publicity. But it is also a way for early-stage investors such as VC/PE to exit. Higher valuations are a strong incentive to do an IPO from the capital raisings point of view and the VC/PE perspective.

However, making a company public today is a long process averaging six months in Sweden. It involves and requires the company to recruit a management team that can cope with the mapping process that precedes the listing. It is essential to have a history of figures and to be able to produce a large amount of information in a short time. In addition, management must ensure that the company's processes align with investors' requirements, nowadays including ESG issues.

However, the stock market is quite short-sighted and wants to see constant increases in profits. Once the company's stock is listed, the company's share trades virtually every day. After a listing, a weak share price performance can lead to a competitor enjoying a premium valuation using the arbitrage for a take-over bid. But from a more positive perspective, the company can expand, grow its valuation, and use this to take over competitors. Eat or be eaten, as they say in the animal world.

Are SPACs a forward-looking indicator?

SPACs have dominated the IPO space in the US. According to Pitchbook, there were 19 SPAC IPOs in the US in the first quarter of 2020. The corresponding figure in Q1, 2021 was 317. The SPAC IPO activity has declined until the third quarter of 2021 but is still above the previous year. Interesting is how the capital raised by the SPAC: s has fallen from USD 36.9bn in Q3, 2020, to USD 17.7bn in Q3, 2021. Does that imply that the interest in SPACs has decreased? Or is it more extensive that the overall risk appetite is on its way down?

SPAC IPO activity from Q1 2017 to Q3 2021

The Renaissance IPO Index is an exciting temperature gauge of risk appetite and the level of today's equity valuations. This ETF, listed in October 2013, was trading pretty much in line with S&P 500 until mid-2015 when it started to lag. Right after the Covid-crash, the IPO Index exploded and peaked in February 2021. Below is the IPO Index side by side with S&P 500 and the SPAC Index.

S&P 500, Renaissance IPO Index, and SPAC Index from October 2013 to November 2021

Source: Refinitiv Eikon and Carlsquare

Looking at the SPAC Index compared to S&P 500, one may say that SPACs are not a very good forward-looking indicator.

Higher inflation has had minimal impact on interest rates

The 10-year US Treasury yield moved up from 1.49% to 1.57% last week. The rise was essentially complete on Wednesday after the US inflation figure for October 2021 showed an annualized increase of 6.2 percent. That was the highest increase since December 1990. According to Earnings Insight 285, S&P500 companies used "inflation" in their Q3 2021 presentations. It is an increase from only 109 companies mentioning the inflation word a year ago in Q3 2020.

But the stock market, after initial signs of concern, took it all in stride. There are good reasons for that. In the chart below, we have compared the annual inflation rate in the United States with the 10-year US Treasury bond rate. As can be seen, the dramatic rise in the inflation rate in the wake of the economic recovery that took off from February 2020 has had minimal impact on the 10-year Treasury yield.

In February 2021, the US inflation rate and US 10-year Government Bond yield were 1.68 and 1.25 percent, respectively. Since then, the inflation rate has increased to 6.2% in October 2021. But the US 10-year government bond yield has risen only to 1.58 percent (monthly average for October 2021). The real interest rate has thus changed from minus 0.4 percent in February to minus 4.6 percent in October 2021 (!) It is challenging to imagine that any investor voluntarily put their money in Treasury bonds on these unfavorable terms. The likely explanation for the extremely low pricing of US government bond yields is that some institutions and companies must invest their money in such securities. Some may also believe that today's inflation rate is essentially transitory. To that, you could add that the Fed has manipulated the interest rate level through its large buybacks.

The US annual inflation rate versus US 10-year Government Bond yield from November 2019 to October 2021

Source: Refinitiv Eikon and Carlsquare

Momentum

After last week, one might have the impression that the stock markets are steaming ahead towards a new Christmas rally. That's not quite the case yet. However, cyclically oriented bourses such as the OMX30 have advanced by 0.8% and the German DAX by 0.25% over the last week. Meanwhile, the S&P500 was down 0.3%, while the Nasdaq dropped 0.7% last week.

A nice finish in the US last week, but not very convincing

As US inflation made some investors a little shaky, the bulls returned on Friday, November 12. As shown in the chart below, the index bounced nicely off EMA9. MACD looks a little fishy, calling for cautiousness.

S&P 500 index from April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

Looking at a hanging man-like Doji created in the weekly chart, one is not more convinced.

S&P 500 index, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

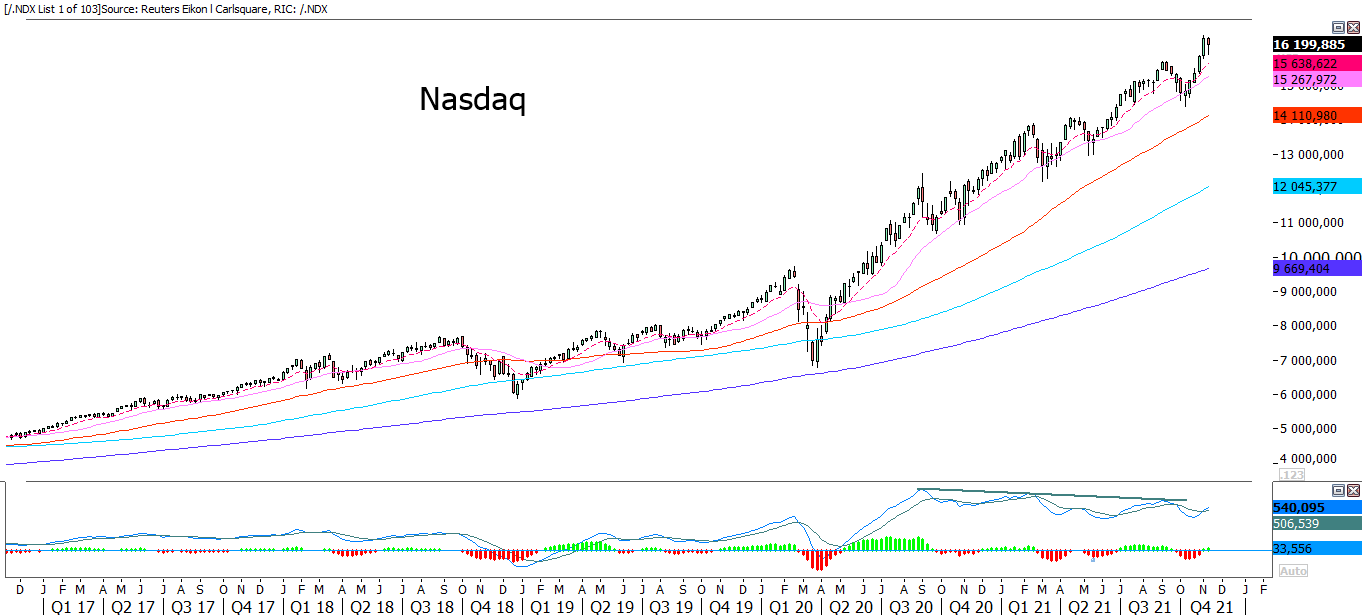

Nasdaq also bounced nicely off EMA9 on Friday.

Nasdaq 100 price graph from April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

In Nasdaq, the negative divergence between the index and MACD is still apparent.

Nasdaq 100, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Can Google set new highs under negative divergence?

Google (Alphabet) set a new intraday all-time high on Monday, November 8 but fell relatively sharply on Wednesday. The share bounced nicely on Friday off EMA9. Is there enough energy left for the Google share to set a new all-time high despite the negative divergence with MACD?

Alphabet, share price graph from April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

Alphabet, weekly five-year share price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

EUR/USD moves in line with the funding futures

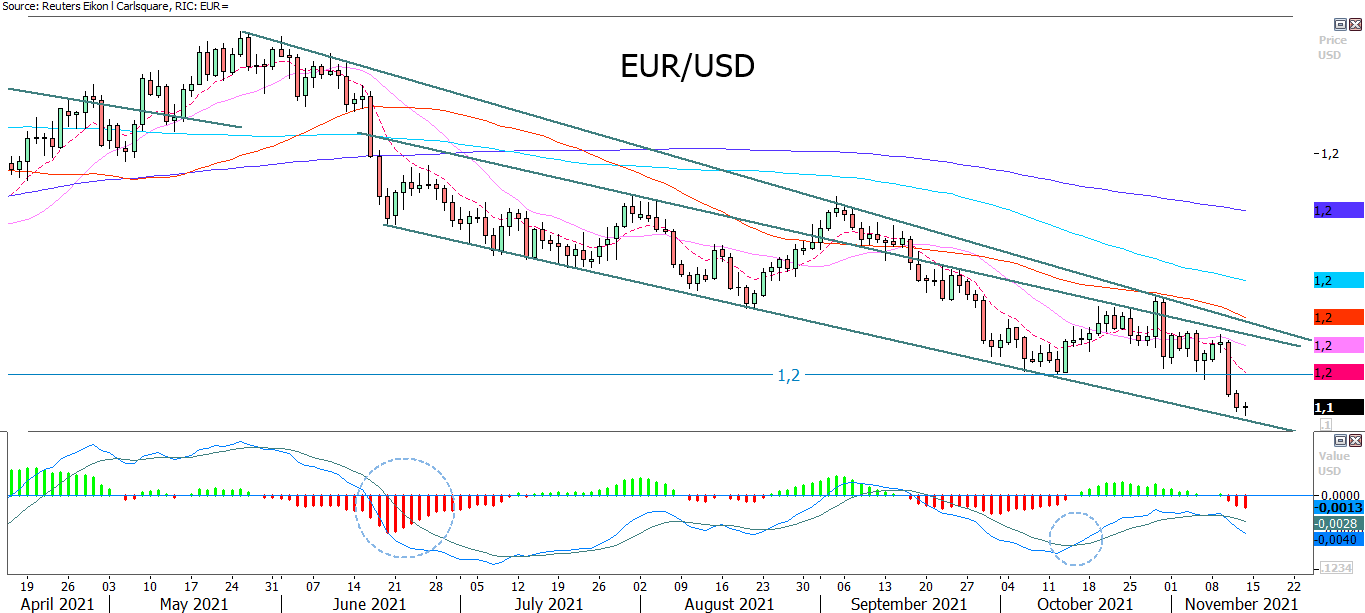

After the CPI figures last week, the funding futures indicate a probability of a rate in June 2022 of 49.6 percent. One week ago, before the latest CPI figures, the corresponding figure was 43.0 percent. USD has also strengthened against the euro, aligning with the market's perception of the future rate hike.

The EUR/USD is currently trading close to the floor of a falling trend channel. See chart below. Note how a Doji was created on Friday, implying uncertainty.

EUR/USD graph, April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, one can see how the currency pair closed well below MA200. Is Fibonacci 38.2 around 1.137 next?

EUR/USD, weekly five-year graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Gold is climbing in tandem – implying inflation may be here to stay

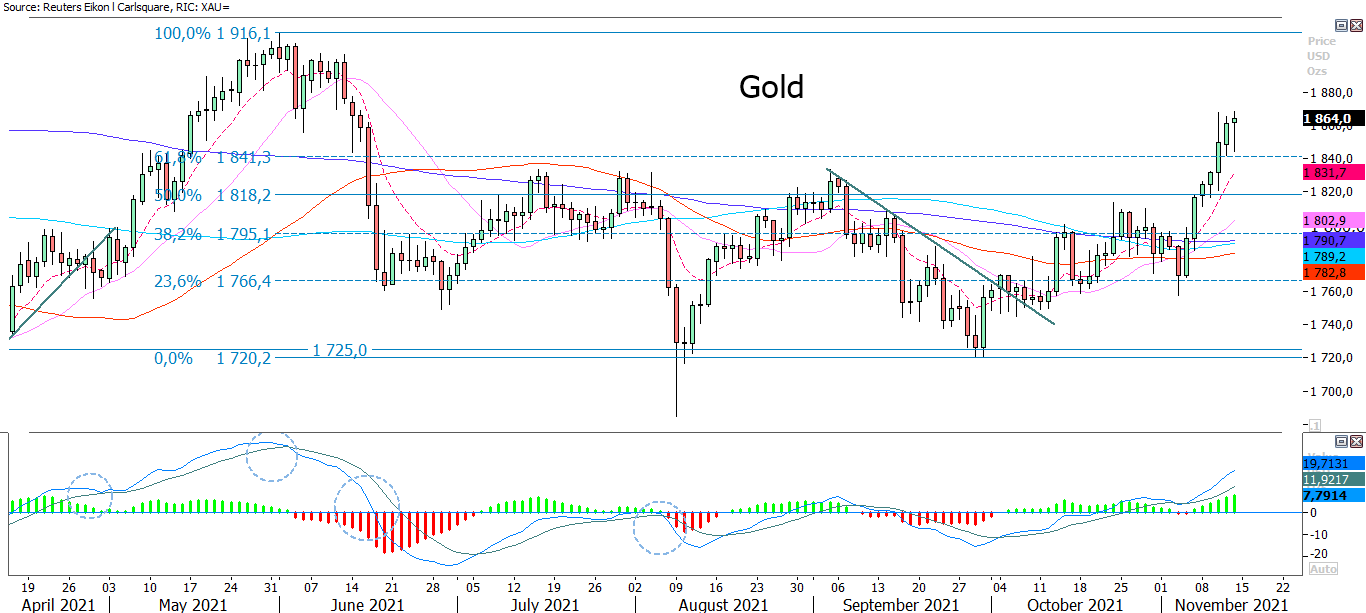

Gold typically strengthens by a weaker USD. However, recently, the gold price has been rising even though the USD has also amplified. Is that a sign of investors taking cover for inflation not being just a temporary post covid and supply issue?

In the chart below, one can see how gold closed above Fibonacci 61.8. Is the previous top from May next?

Gold price graph, April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

Gold, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Is OMXS30 ready to test the previous top?

OMXS30 closed Friday's trading above the local top from October. S&P 500, as well as Nasdaq 100 and DAX, has taken out its previous highs. Is it time for OMXS30 to do the same?

OMXS30 graph, April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

MA20, as well as EMA9, was reclaimed last week in the weekly graph.

OMXS30, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Volvo in good shape

Volvo is trading along with the ceiling of a short rising trend, accompanied by an increasing MACD.

Volvo share price graph, April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly graph, the Volvo stock has broken up from a bullish falling wedge formation. The formation indicates an excellent potential upside to levels above 230 SEK:

Volvo, weekly five-year share price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

A new all-time-high for DAX

DAX is moving slightly upwards in a way that looks almost forced. On Friday, there was a new all-time-high. MACD is losing its steam.

DAX graph, April 13 to November 12, 2021

Source: Refinitiv Eikon and Carlsquare

DAX, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Full name for abbreviations used in previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.