Learn to distinguish between short and long-term effects in the gold price

Gold is often described as a "safe haven" asset. Something you should own during troubled times, and while that is true, the long-term gold case has little to do with short-term events that affect geopolitics or anything else. Therefore, it is important, if you are interested in owning gold, to learn how to separate noise from signals.

Gold is often described as a "safe haven" asset. Something you should own during troubled times, and while that is true, the long-term gold case has little to do with short-term events that affect geopolitics or anything else. Therefore, it is important, if you are interested in owning gold, to learn how to separate noise from signals.

In early January, the gold price rose from about $ 1550 to over $ 1590 in just two days due to concerns over the Iran-US conflict to fall back to previous levels quite directly. This type of behavior is symptomatic of gold and says a lot about how the price moves in the short term in response to situations that can later be dismissed as noise in the larger context. Since then, however, gold has continued to rise, rising as high as over $ 1690 in the noise of the Coronavirus to just the day after, along with all other assets, see the price fall in a total sell- off during Friday, February 28.

Thus, short-term price reactions in the gold price occur because of what we might call noise, or unforeseen and sudden events. It is exactly on those types of occasions that it feels good to already own gold, but it rarely or never gives you a good buying position in the short term, if you do not have ice in the stomach and wait until the price falls back to previous levels again.

But if gold as the " safe haven" is not the biggest reason for owning gold, why would you want to place a yellow stone in the portfolio while waiting for better times for other assets? The answer to the question is, of course, monetary policy relief.

So what drives the gold price in the long term has very little to do with unrest but more so with how central banks around the world (but with perhaps the greatest focus on the US and China) choose to act.

Exhibit A:

Note: Past performance is not a reliable indicator of future results.

The relationship between negative yielding debt and the gold price.

Note: Past performance is not a reliable indicator of future results.

… And another example of the link between monetary policy relief and the gold price. This graph clearly shows that interest rate cuts favor the gold price, something we saw when Powell decided two weeks before the regular meeting to cut interest rates by 50 points in a desperate attempt to stimulate the economy and escape the suites of the virus spread worldwide.

Gold thus may act as a hedge against inflation, and although figures speak of a non-existent one, asset prices seem to tell a different story.

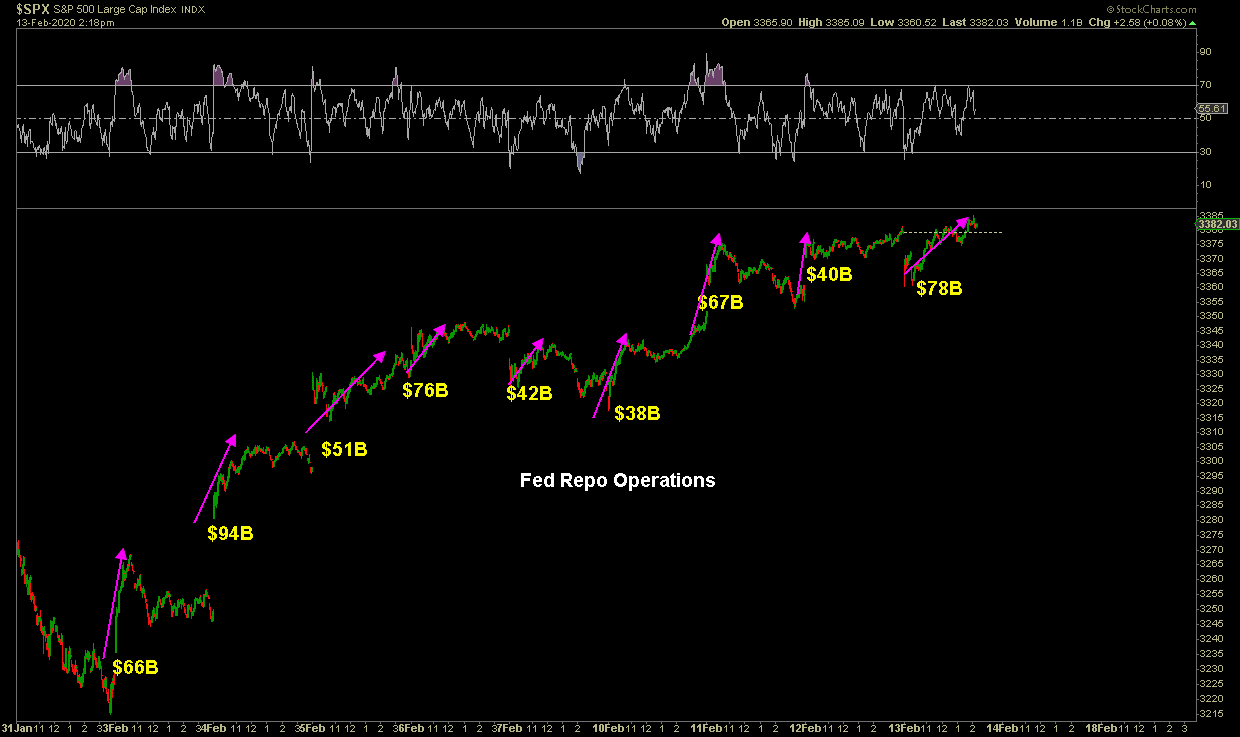

Let me present Exhibit B:

We have become accustomed to the daily liquidity injections in the market. The Fed is printing money and buying assets, or "expanding its balance sheet" (but don't call it quantitative easing for God's sake), which leads to asset inflation. The problem is, though, that in recent months (except for the past two weeks) there has been a happy stock market mood and new ATH after another, we come to a limit where this kind of stimulus no longer works. As a result, the liquidity injected into the market and assets will leak into consumer prices and create consumer price inflation.

However, this is not the first time this has happened. Fiat currencies (issued by a government or central bank) today are a kind of pyramid game built on gold. And what all fiat currencies have had in common historically is that stimulus - money printing - always leads to hyperinflation and that we then have to make a reset of the financial system.

What then does the central banks do about this problem?

… They buy gold.

Exhibit C:

Last year, central banks around the world bought record-high gold. So they are trying to build a hedge against inflation. An inflation that they themselves created.

Capture the signals that central banks send. Is it time to secure part of the portfolio in gold?

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.