Can Fed’s forthcoming tapering provide buying opportunities?

The market is worried about when the Fed will start withdrawing its support to the market, like a disorderly child. The discussion is almost absurd because the Fed continues to grind on with repurchases at a rate of some 90 billion USD per month since July 2020, which drives the stock market upwards.

The market is worried about when the Fed will start withdrawing its support to the market, like a disorderly child. The discussion is almost absurd because the Fed continues to grind on with repurchases at a rate of some 90 billion USD per month since July 2020, which drives the stock market upwards.

Fed total assets and S&P 500

According to surveys from Bank of America, tapering and inflation has replaced Covid-19 as the biggest concern for investors.

The last time the Fed tried to implement a tightening was in 2013. It led to both an interest shock and fall in the stock market, which everyone seems to remember. But if the course of events is studied in a little more detail, a different picture emerges. As usual, it is important to play it cool and read the market correctly. Then situations arise where others only see risks.

In 2019, all minutes of the Fed meetings from 2013 were released. There is an excellent summary by Reuters here:

https://www.reuters.com/article/us-usa-fed-2013-timeline-idUSKCN1P52A8

Already at the beginning of the year of 2013, the discussions were hot in Fed about when and how the support should be withdrawn. But nothing was said outwardly in the communication.

It was not until May 22 of 2013 in a congressional speech that then-Fed chief Ben Bernanke mentioned the possibility of withdrawing support in the following words:

“If we see continued improvement and we have confidence that that’s going to be sustained then we could in the next few meetings ... take a step down in our pace of purchases,” Bernanke said.

If you just read the text, you can see it as a speculation about withdrawing support, if and only if the economy continues to improve. As for the time, it is during future meetings, however unclear in time. And even the scope is unclear as he says: “take a step down on our pace of purchases”.

In other words, it is a very loose statement that still created panic in the fixed income market.

TNX, US 10 year yield

Within five months, the 10-year US government bond yield rose from 1.6 to 2.9 percent, which is one of the strongest interest movements ever.

Interest rates should rise when the economy is performing well, which it did in 2013. But this time it became a double effect for the fixed income market. On the one hand, interest rates began to rise since the Fed forecasted a strong economy ahead. But the trigger was that the fixed income market imagined a flood of bonds that would be for sale in the coming months. It is understandable that everyone is trying to run away when the train runs amok and unexpectedly change lanes. Seldom has so few cautious words had such a powerful impact on the market…

The market reaction also surprised the Fed. During the subsequent Fed meeting on 18-19 June 2013, Bernanke received a restraining order to go out and calm the market. The latest economic statistics had not been as bright as before either.

“Policymakers, worried about more communications snafus on asset purchases, had Bernanke use his press conference to hone the point they felt markets were missing: That any changes to bond buys would depend on the economic outlook, and that decisions about bond purchases were distinct from those concerning interest rates.”

TNX and S&P500

It did not take much to calm the stock market. The Fed continued to pump money into the market, spilling over into the stock market. On the other hand, the effect seem to have been more detrimental to the bond market, where interest rates continued to rise. But interest rates will rise if the economy improves and the stock market rises. It is as we always claim that rising interest rates are not the threat. It is rapidly changing interest rates (in both directions) that can be detrimental to the stock market.

Our conclusion on this right now, is that all discussions and speculations about tapering can be seen as noise. The Fed has put itself in a corner that will be very difficult to get out of. In the coming months, a number of test rockets will be released to see if the market is riped for reduced support. Eventually, you will get into a situation where it is psychological right to cut back on support. But we are not there yet and as long as the Fed’s balance sheet grows, the stock market also continues to benefit. In other words, when the market if frightened, buying opportunities are likely to arise.

The employment figures for the United States presented on Friday 4 June once again illustrated the picture of a dysfunctional labor market. Expectations were for 650,000 new jobs having been created, while the outcome was 559,000 new jobs. It is still not as bad as last month when the miss was epic. In addition, US employers would have liked to hire additional staff if they only had find enough people.

The market swallows this bad news since weak numbers mean continued financial support.

The relation between growth in number of new jobs in the United States and performance for the S&P500 index continues to be relative strong. This is even though the stock market has continued to outperform due to other reasons such as increased liqudity in the market.

Note: past performance is not a reliable indicator of future results

In September, the current unemployment benefits is about to expire. It is a threat to the market since it opens a trapdoor for all those who today do not have the strength to look for work. This in turn can lead to social unrest. Unfortunately, we will have reason to return to this theme.

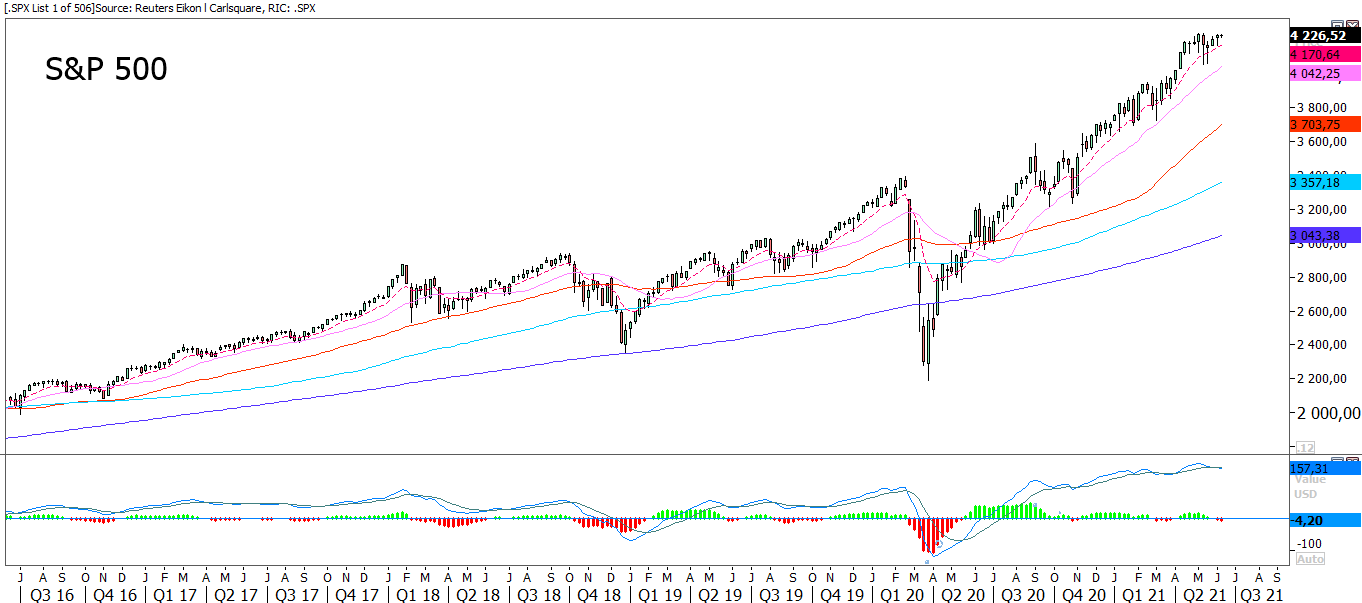

S&P 500 is gaining ground on its previous top. Momentum is once again upwards sloping and the odds of a new ATH has improved. As we have mentioned earlier, it is important for the trend that a new high can be set.

5 year

Note: past performance is not a reliable indicator of future results

Also, tech-heavy Nasdaq had a nice move upwards on Friday 4 June. Can the 13 800-level and the previous top be broken?

5 year

Note: past performance is not a reliable indicator of future results

Tech-heavy Nasdaq has been more sensitive to movements on the debt market. As can be seen in the graph below, the 10-year US government bond rate fell on Friday. A continued decline in the interest rates will support the upwards movement for stocks in general, but especially growth companies including the tech sector.

5 year

Note: past performance is not a reliable indicator of future results

But index heavy constituents such as Apple is under pressure. The share is currently testing MA20, but momentum is negative and falling, which can be seen in MACD. Nevertheless, MA200 has managed to hold for the three tests since May:

5 year

Note: past performance is not a reliable indicator of future results

Alphabet on the other hand is likely to improve its advertising revenues as the economy keeps improving. The share is also testing a previous high:

5 year

Note: past performance is not a reliable indicator of future results

Gold has seen some good intraday volatility during the last two days. During Friday 4 June, the metal managed to stay above MA20, but EMA9 still remains to be taken back. Also note how MACD has generated a weak sell signal.

5 year

Note: past performance is not a reliable indicator of future results

So far gold has been as a good hedge against inflation concerns. But the correlation with USD is also strong. Below is EUR/USD. As shown, the currency pair did not manage to take back MA20 on Friday 4 June. MACD has generated a weak sell signal. A continued decline in EUR/USD is bad news for the gold price.

5 year

Note: past performance is not a reliable indicator of future results

But a weakening euro against the USD would be in favor for the German DAX index, that is currently leading the race in the western world. As shown in the graph below, another ATH was set during Friday’s trading:

5 year

Note: past performance is not a reliable indicator of future results

In Sweden, the OMXS30 index is struggling to set new highs. Note however how momentum has turned and is now rising. The index composition with focus on cyclical stocks is likely to work in favor of OMXS30 performance:

5 year

Note: past performance is not a reliable indicator of future results

Risks

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.