Who should buy all the shares?

Many people are betting that the worst are behind us and that it is the right time to go against the falling market. Since 2008-2009, it has always been the right tactic to go against the market and buy on all the dips.

Many people are betting that the worst are behind us and that it is the right time to go against the falling market. Since 2008-2009, it has always been the right tactic to go against the market and buy on all the dips.

The graph above shows the S&P500 since 1992. Note the peaks in 2000 and 2008. With the 2008-2009 crisis, the Fed introduced a very expansionary monetary policy to support the markets. President Trump topped this policy by lowering corporate taxes, which further boosted development. This expansionary period coincided or rather strengthened an already ongoing trend in the fixed income market, which meant that interest rates had fallen steadily since 1982.

The red rising line is the S&P500 while the black falling is the interest rate. Declining interest rates are a strong driver of rising prices equities, as low interest rates show a heard supply of capital. Low interest rates also make it increasingly attractive to buy shares with stable returns. This also indicates that shares should now be cheap. Interest rates continue to fall, which justifies a rising P/E-figure.

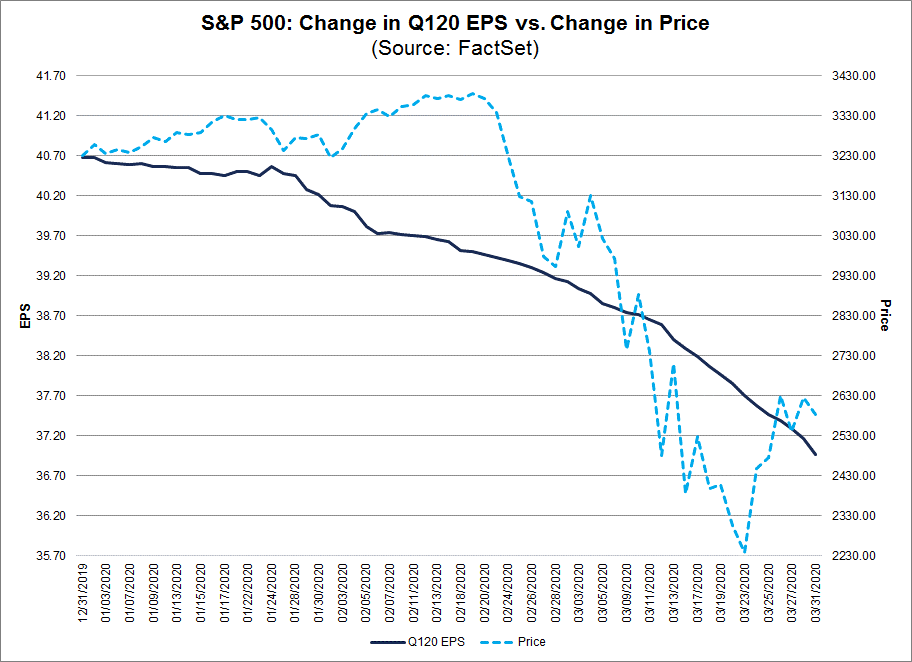

The graph above shows that the S&P500-index has fallen at roughly the same rate as profit expectations in the United States were downgraded for Q1 2020. Already here you should pull your ears. The major effect on corporate profits should appear during the current and coming quarters, i.e. Q2 and Q3 2020.

This slowdown in the economy should be at least as serious as the 2008-2009 financial crash. The graph above shows the effect during these quarters, which resulted in downward adjustment of about 30 percent. So far, profit expectations have been adjusted down by 10 percent in the US for Q1 2020 but are expected to hit significantly more in Q2 2020. This is unknown territory for most analysts, so it will be very difficult to get right into the forecasts without guidance from the companies. We have so far seen very few guides from the companies. This is since it is very challenging for them to calculate the effects.

That then as many fundamental analysts go and say it is cheap, we think is a bit daring. It is possible that they are right, but we think it is too early to state that the danger has disappeared. The graph above shows the P/E figures for the S&P500-index since 1970. The P/E figures have fallen to 19.3 now, but it is based on historical gains.

But the most interesting are not the values. Most people in the stock market do not understand that valuations are based on relative values and historical averages. When you state that a company is inexpensive because it is, for example, traded at P/E 10 or 15, this is based on that the company or the sector usually trades at higher P/E figures. But there is no natural law that determines to which P/E ratio a stock should be traded.

Everything is about supply and demand. There is where we start to get a little worried. We know that the Fed has been sweeping the market since 2009. The trade that has existed since then is that low interest rates have created demand for corporate bonds. The companies that have issued these have either used these to create better leverage, acquisitions or expansion. But especially in the US, the money has also been used to repurchase existing shares. This has created an underlying buying pressure in the market, which has driven up the demand for shares and thus the price of shares.

Now that the Fed more than doubles support purchases in one go, we should probably have the same effect. Our immediate response is that this is positive for the stock market, because we know that a large part of these support will be sought in the stock markets. But we don´t really know how.

This is what demand looks like since the last crisis from different buyers. Note that pension funds in the US have been net sellers, which surprises us. These are supposed to continue to be net sellers. Now with the rapid crisis there are also A-funds that most foreclosure assets to pay out support to unemployed members.

Foreign investors are expected to disappear at least in the short term. ETFs have run the course but we have difficulties in seeing that new ETFs will be launched in the near future. Here we have identified a possible purchase pressure. Bank of Japan purchases directly in the stock market via ETFs. If the stock market goes down too much to create confidence in the markets in common, it would be logical for the Fed to start buying there as well. They are dangerously close already when the Fed started buying on the corporate side to save the market.

Looking on the graph, this is a major source that, in addition to ETFs, has accounted for almost the entire net effect, and it is companies that repurchase their own shares. This has been achieved through profits in the own company or through corporate bonds. If a manager has had an option program linked to the share price, it has been an almost foolproof way for management to both emerge as heroes and at the same time draw their own profit on the system.

But with the current implosion in the world economy, few companies know if they will deliver profits in the next few years. If they take out loans in an already strained market for corporate bonds, the money will primarily be allocated to their own operations and only in exceptional cases to buy back their own shares.

But according to the US state directive on aid loans, share repurchases are prevented for 12 months for companies wishing to apply for them. According to the Goldman Sachs Buyer Program Dealer box, demand has fallen rapidly.

According to Goldman´s forecast, the repurchases will be halved in 2020 compared with 2019. Note that the repurchases will then be down to the level of 2008-2009. We cannot not see that there is anyone other than the central banks that can balance up the purchasing power in the stock market as the repurchases decrease and the usual buyers such as oil countries, pension funds, A-funds and all others need to free up capital. When it looked dark in the beginning of 2009, we wrote that there was no real light in the tunnel. But they began to lean on the central banks, especially the Fed, to start buying bonds. The day they did it was also the time to buy in the stock market.

This time, buying in the bond market is not enough. Rather, it´s time to track the Fed on the day they start buying shares directly in the market. But, as we said, they probably do like Japanese BOJ and rather buy ETFs.

Until then, it is important to keep your ears to the rail and avoid being overtaken by any sudden train coming.

S&P 500 did not manage to break above the falling MA20. The short-term trend is thus still on the decline. Note also how the faster EMA9 has flattened out meaning that momentum is fading:

Support is found around Fib 23.6 at 2 473. In case of a break below, previous local low from March may be a next.

Nasdaq is also trading below a falling MA20. As well as S&P 500, Nasdaq is trading close to its support. EMA9 is once again flattening out:

In the daily graph shown below one can see how the OMXS30 index made a brave attempt to break above MA20. However, the index closed the week near its low levels on a weekly basis, below a falling MA20 as well as a falling EMA9:

Note how the 1 400-level on the downside is still intact.

Retail operations are taking a hit and H&M is no exception. On Friday, the company released its sales figures for March, which were down by 46 percent. The H&M share also declined on the news failing to break above MA20:

The next level in target is a previous local low from March.

The German DAX index was also under pressure last week and like OMXS30 it failed to break above a falling MA20. Fib 23.6 is still in play. The next level of support can be found around the 9 300-level. A break below, and the risk for a further set back to previous low from March increase:

Last week, the USD regained strength against the Euro. As shown below, EUR/USD closed below Fib 23.6:

Momentum is in a falling trend as shown by MACD. The next level on the downside can be found around 1,06.

A stronger USD work against rising gold prices. However, in the daily graph gold still managed to close last week almost unchanged and above Fib 61,8:

The Gold price is now facing resistance in form of a falling trendline. A break above and the next level can be found around 1 645.

As shown in the graph below, the Oil price (WTI) closed Friday´s trading above MA20. EMA9 is also once again rising. The next level on the upside can be found around 30 USD/barrel:

However, there were rumors on Saturday that the planned meeting on Monday between Russia and OPEC has been postponed. This as Russia and Saudi Arabia is disputing on who is to blame for the plunge in oil prices.

Bitcoin is trading above a rising EMA9 as well as MA20. As can be seen in the MACD, the momentum is increasing but is still in negative territory. Resistance is found around 7 166 where Fib 50 meet up:

Risici

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.