US job growth illustrates the road to recovery

For August and September 2021, Wall Street investors were disappointed about the job figures of 235,000 and 194,000 new jobs. Therefore, it was a great relief for the stock market that the October job figures released on Friday, the fifth of November, were more vital - 531,000 new jobs have been created compared to expectations of 280,000.

In this weekly trading note from Carlsquare, we elaborate on the following topics, indices, and stocks:

- US job growth illustrates the road to recovery

- Consumer confidence and air traffic follow

- Equity and fixed income investors have different views

- EUR/USD yawned and closed unchanged

- S&P 500 is flying. When is it time for a break?

- Nasdaq is flying even higher

- Google has reached the stratosphere

- Tesla in the mesosphere, an opportunity to get out, or is Mars next?

- OMXS30 is back in the atmosphere

- Oil in the thermosphere compares to the weaker indices

US job growth illustrates the road to recovery

For August and September 2021, Wall Street investors were disappointed about the job figures of 235,000 and 194,000 new jobs. Therefore, it was a great relief for the stock market that the October job figures released on Friday, the fifth of November, were more vital - 531,000 new jobs have been created compared to expectations of 280,000.

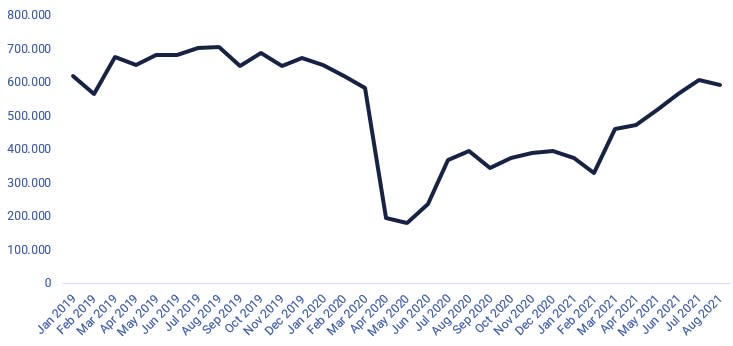

Job growth was widespread to leisure, hospitality, professional and business services, manufacturing, transportation, and warehousing. The only exception was, like September, employment in public education, which declined in October. Unemployment in the United States fell 0.2% to 4.6% in October 2021. However, this level is higher than before the Covid pandemic in February 2020, when unemployment in the US stood at only 3.5%. We have added the cumulative changes in the number of jobs created in the US in the chart below.

US Non-Farm Payrolls cumulative changes from the thirtieth of November 2019 to the thirty-first of October, 2021 (000)

Source: Refinitiv Eikon

The significant drop was 20.5 million jobs (!) temporarily lost due to the Covid restrictions in April 2021. Cumulatively as of the thirty-first of October, 2021, the US is still at minus 3.8 million jobs compared to the twenty-ninth of February 2020. It equals seven more good months, like October 2021, before the labor market has fully recovered to pre-Covid levels.

Consumer confidence and air traffic follow

Consumer confidence in the United States rose in October after being weak in the previous three months. We have seen increased sales for retail, banking, and warehousing service companies. Moreover, the US CPI Index stood 5.4 percent higher as of the thirtieth of September 2021 than one year earlier. Inflation is a symptom of bottlenecks in the global supply system.

Another indication of the recovery in the economy is air traffic illustrated in the graph below. As can be seen, even here, we are not back to 2019 levels yet.

Total US flights operated from January 2019 to August 2021

Source: Bureau of Transportation.

Equity and fixed income investors have different views

The S&P500 index advanced 2.0% last week (1-5 November), with the Fed's interest rate announcement on Wednesday, the third of November playing the most significant role in the rise. The US 10-year Treasury yield has fallen back the last two weeks. At its top from 1.696% to 1.455% on the fifth of November. Meanwhile, the US experienced an annual inflation rate of 3.9% in the third quarter of 2021. So even if the inflation rate flattens out from now on, we have sharply negative actual interest rates. It supports the value increases of assets like stocks and real estate. Not so fun for bond investors, though.

The United States CPI index from the thirty-first of October, 2019, to the thirtieth of September, 2021

Source: Refinitiv Eikon

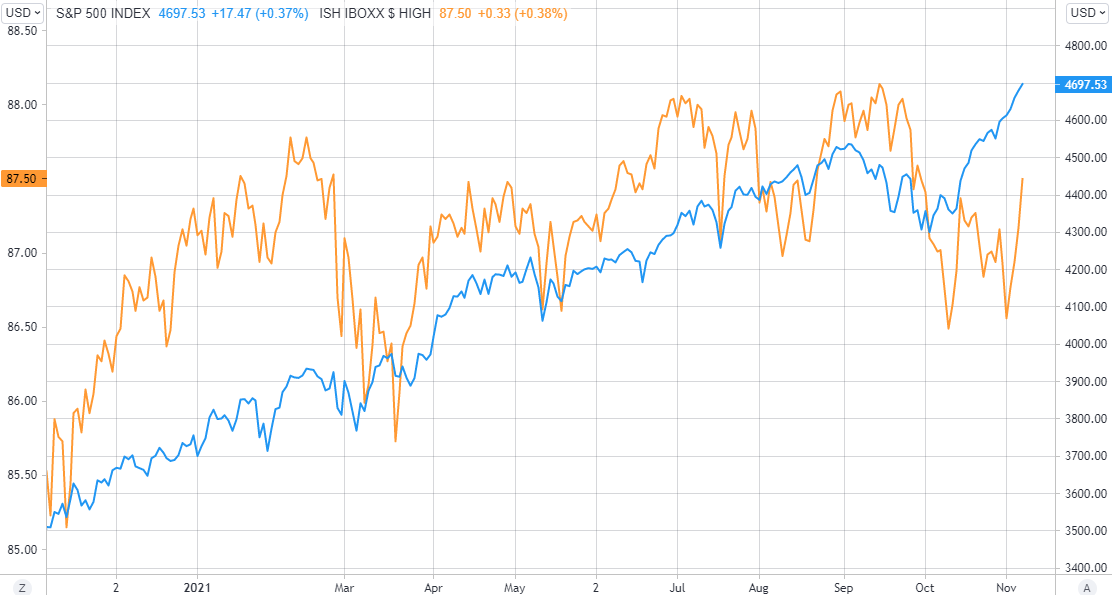

In recent months, we also note that the S&P500 index has performed stronger than HYG (the junk bond ETF). The equity and fixed income markets have slightly different perceptions and appetites for risk now. In the long term, the S&P500 and HYG should correlate quite well. With the interest rate drop on Friday, the fifth of November, this spread should start to decline again

HYG and S&P500, November 5, 2020 to November 5, 2021

Source: Refinitiv Eikon

EUR/USD yawned and closed unchanged

The EUR/USD did not think much of the last week's macro statistics and closed the week near unchanged.

EUR/USD, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

However, it's in the weekly graph where "it all goes down." As can be seen, the currency pair is clearly under pressure pushed downwards by EMA9 under a falling momentum, as visualized by MACD. MA200 has so far managed to stay strong. In case of a break, the next level is around 1.145, where Fibonacci 50 meet up:

EUR/USD, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

S&P 500 is flying. When is it time for a break?

S&P 500 index has been flying since early mid-October. Since the first of October, the index has been up 7.8 percent. Year to date, the index is up just above 25 percent. RSI is on overbought levels, though that is not a sell signal stand alone. On Friday, a scary-looking Doji was created, indicating uncertainty on the next move. A break is well needed.

S&P 500 index graph, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

S&P 500 index, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Nasdaq is flying even higher

Nasdaq has also been flying. Since the first of October, the index has been up 10.6 percent and has thus outperformed the broader S&P 500. The gap between the two indices started when the rates turned south.

Percentage development since the first of October, 2021: S&P 500, Nasdaq 100, and US 10 year yield

Source: Refinitiv Eikon

Nasdaq has outperformed S&P 500 year to date by close to 27 percent, compared to S&P 500's 25 percent. But again, RSI is on overbought. Moreover, a scary-looking Doji has been there since Friday.

Nasdaq 100, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

Nasdaq 100, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Google has reached the stratosphere

Among the FAANG-companies, Google or Alphabet is the winner by being up close to 70 percent. Alphabet is close to making the second-best performer in the FAANG-group, Facebook, or Meta Platform look silly.

Percentage development, YTD: FAANG-companies and Microsoft

Source: Refinitiv Eikon

The chart below shows that Google has created a secondary short rising trend, parallel to the longer rising tendency. The share is now trading close to the ceiling of the more temporary movement. On Friday, another Doji came in place. Thus, uncertainty is also the theme going into Monday's trading for Google.

Google share pricer graph, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

Google share price, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

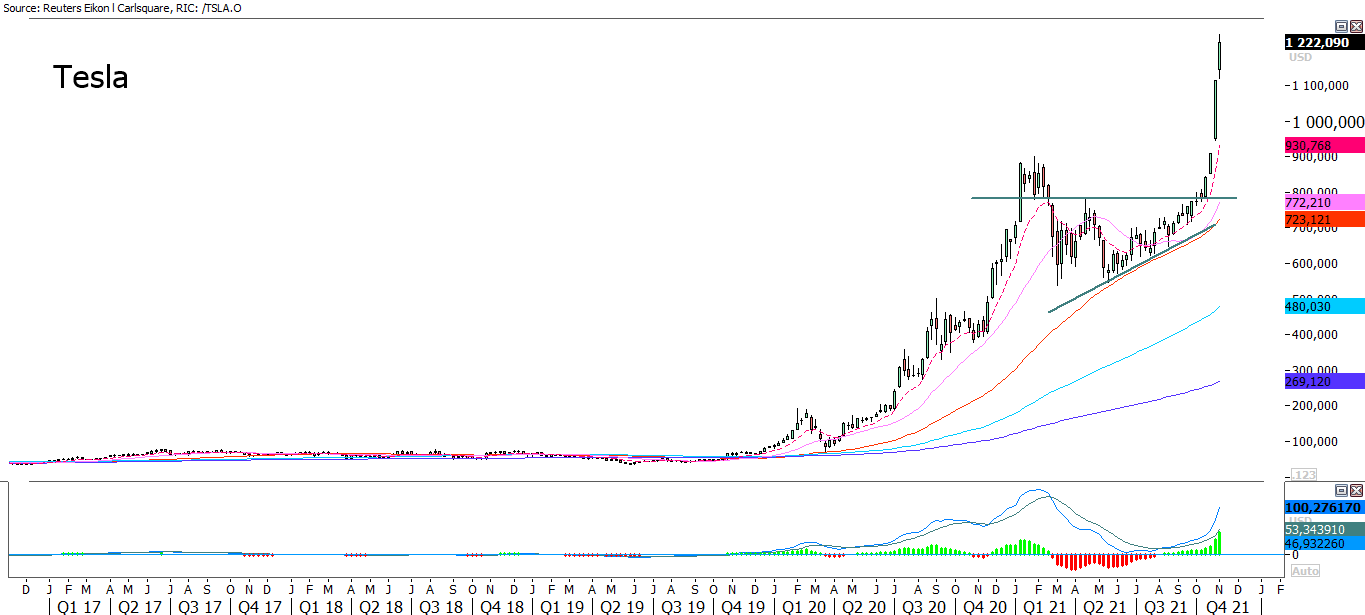

Tesla in the mesosphere, an opportunity to get out, or is Mars next?

Given Tesla's recent rally, it has now reached the mesosphere. However, that is not good enough if Elon Musk wants to go to Mars.

Percentage development, YTD: FAANG-companies plus Microsoft and Tesla

Source: Refinitiv Eikon

But for investors, it may be time to consider winding down on its positions and realize some profits. Based on the last two trading days, it looks like some investors also are doing so.

Tesla share price, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

Tesla share price, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

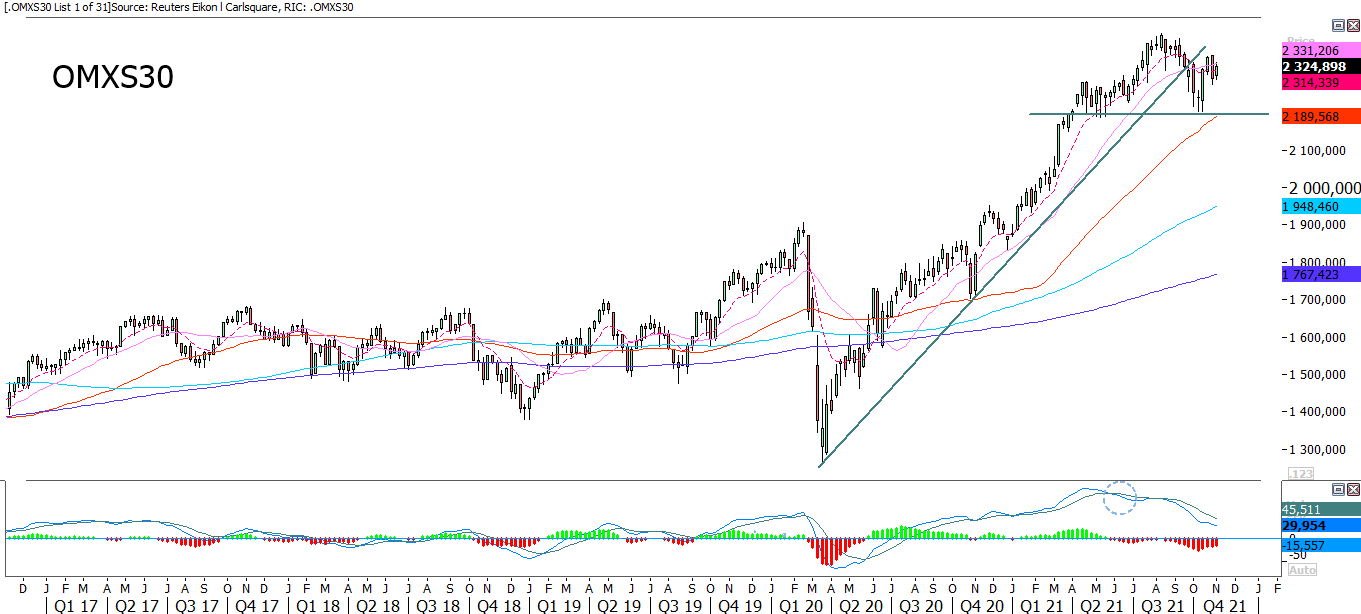

OMXS30 is back in the atmosphere

Being ahead of most other major indices, OMXS30 lost its 1st place by the end of October. Now, both S&P 500, French CAC 40, and Italian FTSE MIB are ahead.

Percentage development, YTD: OMXS30 and other indices

Source: Refinitiv Eikon

However, last week OMXS30 attempted to retake MA100, but it ended up with two Dojis implying uncertainty. Also, as no move came after the early close in Stockholm, the uncertainty remains. However, both EMA9 and MA20 are rising and supporting from below.

OMXS30 graph, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

OMXS30, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Oil in the thermosphere compares to the weaker indices

Brent oil has flown off to the thermosphere compared to the weaker indices, Shanghai's, SSEC, and Nikkei. Year to date, oil is up more than 60 percent.

Percentage development, YTD: OMXS30 and other indices

Source: Refinitiv Eikon

Last week, the oil price dipped but bounced nicely close to Fibonacci 23.6 on Friday. A break above EMA9 and MA20 would be a trigger for a test of the previous top. However, MACD does not look so happy.

Brent oil price graph, the fifth of April to the fifth of November, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, one can also see how the oil price bounced nicely of EMA9.

Brent oil price, weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risici

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.