The right price for oil

The interest of private individuals to buy oil has grown exponentially as the price has fallen. This can be seen among other things at the online broker Robinhood. The dip buyer mentality has spread from the stock market, so for whatever fundamental reason, private investors think lower prices mean a discount buying opportunity, “a sale!”, that will soon be followed by a rapid recovery. However, the stock market has time on its side; Nominal prices follow the money supply up eventually and there is no end date for a share. Many will learn the hard way that it does not work the same way for oil.

The interest of private individuals to buy oil has grown exponentially as the price has fallen. This can be seen among other things at the online broker Robinhood. The dip buyer mentality has spread from the stock market, so for whatever fundamental reason, private investors think lower prices mean a discount buying opportunity, “a sale!”, that will soon be followed by a rapid recovery. However, the stock market has time on its side; Nominal prices follow the money supply up eventually and there is no end date for a share. Many will learn the hard way that it does not work the same way for oil.

For starters, there is not just a single price for oil, but different forward contracts with the end date of the 20th every month. You can today choose to pay about $ 24 per barrel for the August 2020 contract, or for example. $ 30 for the February contract 2021. As the date of delivery approaches, you can sell the futures at the price applicable at that time. Now it is in practice the June contract and it is traded at just under $ 19. And in the chaos a few weeks ago, the spot price fell where the person who finally sat with the contract for delivery on hand to minus $ 40 per barrel. This meant that anyone who did not want to take delivery for not being able to or can handle the physical oil had to pay $ 40 per barrel to get rid of the obligation to receive the oil. Some of these may have paid $ 20 a barrel a few weeks earlier, believing that the oil was too cheap due to corona worries and would soon bounce back to 30. Instead of a 50% profit, they had to book -300%, or $ 60 in a loss per contract.

The basic problem is that there is more oil produced than consumed, when the world is stationary due to the corona pandemic. For example, in the United States, 40% less gasoline is currently used than normal. When oil stocks on land and in boats at sea are full, the situation becomes difficult. The producers do not want to choke their sources of oil because it is extremely expensive. Sometimes it is not even possible to start the sources again, which keeps them open at almost any price. When the recession after Covid-19 is over, the demand will return and prices will rise to levels that offset production costs. Unfortunately, as an oil buyer today, you do not get part of that upturn because the contracts reach their end dates before that.

An ETF can today own e.g. the next three months' oil contract, June-August, for an average value of $ 21.37 per barrel. If these are to be replaced by July-September, the fund must pay $23.66 per barrel. It is this price difference for different contract end dates called contango. With the current price structure, the fund can only afford to roll 90% of its holdings. As a co-owner of the fund, after rolling, you will own 10% fewer barrels of oil. This means that if the price rises by less than 10 per cent per month, you will lose your oil investment. This goes on month after month as long as you own shares in the ETF or you roll the futures in front of you. It becomes even worse if part of the holding has to be rolled into a position like April 21, when it was forced to pay up to $ 40 / barrel to get rid of the front month contract (May 2020) and at the same time pay $ 10 / barrel for June. Fortunately, very few contracts were traded that day.

The situation is partly because the producers refuse to adapt to reality, and partly because uninsured private individuals mistakenly believe that if the spot price rises from levels below $15 to long-term motivated levels of $ 30-45 within a year or two, they will "easily" double the money. The truth is instead that with the current futures curve, which lasts as long as it is difficult to get hold of oil stocks, the price can rise by 5% a month while you lose 5% a month. And as long as the oil producers sell futures contracts with the full intention of delivering the oil, to private individuals and ETFs who cannot receive the oil, there is a risk of reprisal of the chaos in the May contract, although negative prices should not be repeated after all.

If you want to make money on oil you have to do as the producers and sell as long futures as you dare. You get $ 31 for the March 2021 contract. If the spot price, which currently stands at $ 18.77, this spring is lower than $ 31, you make a profit. Another way to put it is that if you buy the March contract for $ 31, the 9-month spot price must be 65% higher than today's $ 18.77 level just for you to go straight up the deal. If you instead roll monthly for 9 months, it seems to be even more difficult “contango uphill” as an oil investor, whether you invest directly or through an ETF.

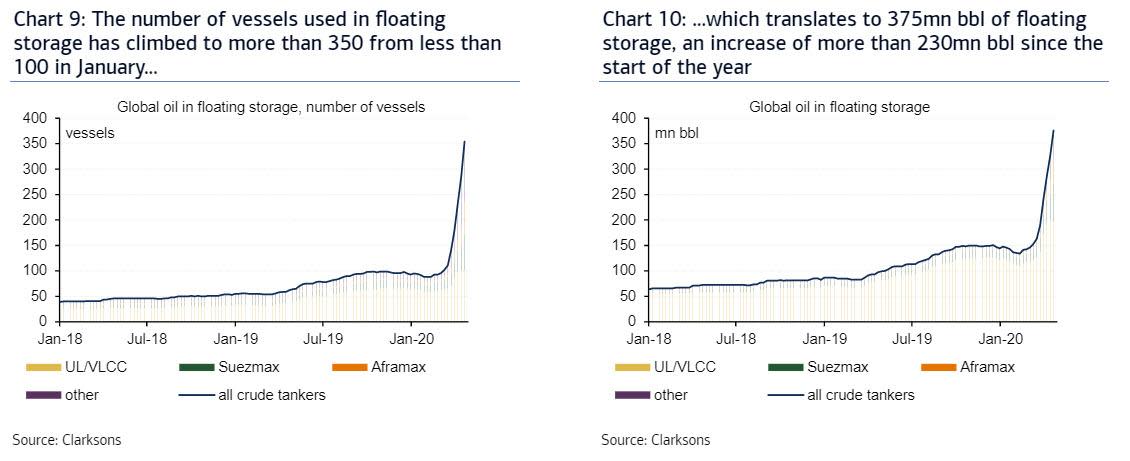

The Contango problem is significant, especially for those individuals who do not understand what they are buying or what it takes to go plus, but to a large extent it is a storm in a water glass. Only a few thousand contracts, i.e. a few million barrels of oil, were traded at negative prices. This involved only a few tens of millions of dollars in unexpected losses. Contangon for the most important release months is limited by the cost and storage capacity. Most of the excess oil can always be stored by re-prioritizing the use of oil tankers. There are, for example, 800 VLCC boats that theoretically can store 1.6 billion barrels. This corresponds to more than six months of over-production of 8 million barrels per day (which is 10% of the production rate in 2019). However, according to Clarksons, 375 million barrels are already stored at sea. But with some luck, the economy has bottomed out within six months, plus some of the most expensive sources have been shut down.

Right now it costs just over a dollar per barrel a month to rent an oil tanker if you sign a one-year contract. That is why the one-year contracts, i.e. for June 2021, cost $ 13 more than June 2020. When the panic was worst on April 21 this year, the short-term rent for a VLCC tanker rushed to the equivalent of $ 4.50 per barrel per month. Can it really get worse then again when everyone is prepared? If not, the price difference between June and July should not be greater than $ 4.50 per barrel. Since it is at $ 3, there is no obvious location, but a June-July contango of over $ 9 a few weeks before the ransom should be able to attract enough storage space to get the price to bounce upwards. If you are in the mood to store oil yourself, a standard garden pool of 8x4x2 meters holds 400 barrels of oil. You can buy the June contract at $ 18.77 and at the same time sell the September contract at 25.64. You fill the pool when the June contract goes to delivery and then you deliver the oil three months later. Your profit will be $ 2750, or $ 27,500 for having oil in the pool all summer long.

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.