The index composition makes the difference

This week we look at the composition of three major stock market indices; the S&P500 (New York Stock Exchange), the DAX (Frankfurt), and the OMX30 (Stockholm). We start with the S&P500.

In this weekly trading note from Carlsquare, we elaborate on the following topics, indices, and stocks:

- The index composition makes the difference

- S&P500 driven by growth companies

- US banks helped improve the sentiment, but more reports to come

- Is S&P 500 set for the previous top?

- Nasdaq got stuck

- Amazon

- The dominance of cyclical and value stocks in DAX

- Nice move in DAX, but now at a strong resistance

- OMXS30, for value investors

- OMXS30 testing MA100

- Boliden is gaining from rising copper

- Copper is flying

- Weaker USD gives support to copper

The index composition makes the difference

This week we look at the composition of three major stock market indices; the S&P500 (New York Stock Exchange), the DAX (Frankfurt), and the OMX30 (Stockholm). We start with the S&P500.

S&P500 driven by growth companies

The US stock markets account for between 50 and 60 per cent of total global market capitalization. It is perhaps somewhat surprising that the average S&P 500 company derives between 60 and 65 per cent of its revenues from North America, including the US, which is the world's largest economy (24 per cent of global GDP). Moreover, the remaining 35-40 per cent that a typical S&P 500 company exports go to neighbouring Latin America, Europe and Asia. But then we are talking mainly about industrial and consumer goods companies. The big US exporters are primarily in the technology sector, with various hardware, software, and other services sold worldwide.

The S&P 500 is admittedly a broad index with 505 companies. Nevertheless, six technology companies represent 25 per cent of the index's market capitalization. Several well-known FAANG stocks such as Facebook, Amazon, and Alphabet (Google) are in the top six in the list of companies with largest market capitalization. But there are also more mature growth companies like Apple and Microsoft. At the other end of the scale, Tesla with sky-high expectations discounted in the company valuation.

There is breadth in the S&P500 index, as shown by the 490 smallest companies in terms of market capitalization, which account for just under 65 per cent weight in the index. Moreover, among the fifteen most significant companies, investment companies, banks, consumer goods, and healthcare companies are also found there.

The 15 largest companies in the S&P500 ranked by market capitalization

Source: Refinitiv Eikon

One consequence of the S&P500 index now has a high proportion of growth companies is that the overall market capitalization becomes quite sensitive to any changes in the interest rates. The value of growth companies' projected earnings well into the future becomes more valuable discounted at a lower discount rate. But it is important to remember that, given today's low-interest-rate environment, the risk-free interest rate (typically equal to the interest rate on a five-year government bond) represents a relatively small part of the total return requirement. The general market risk premium is currently much larger than the risk-free interest rate component. This market risk premium varies somewhat over time and can probably be read indirectly via HYG (junk bond ETF).

US banks helped improve the sentiment, but more reports to come

S&P 500 index advanced last week by 1.8 per cent. The week began with a decline, but it turned upward starting on Wednesday, October 13.

Four US banks reported their results for the third quarter of 2021 above expectations on Thursday, October 14, which helped strengthen the stock markets in the US and indirectly other markets. More positive sentiment was also seen on HYG, showing a risk appetite for junk bonds. The US 10-year Treasury yield fell back from a high of 1.63% to 1.57% at the close on Friday, October 15. It happened even though inflation data in the US had continued to show a worryingly high rate earlier in the week.

US 10 year yield graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

Last week, another 20 companies in the S&P 500 index reported six of which were significant banks. Now a total of 41 companies have reported their Q3 2021 results. 83% of the reports have shown better-than-expected results, while 88% have reported higher revenues than analysts' forecasts.

Analysts have revised earnings estimates for Bank of America and Wells Fargo by 7% each in the last 30 days, giving proof that the banks’ Q3 2021 reports were strong.

Now the reporting season shifts from banking reports to more of Technology, Consumer Goods, and Industrials such as Johnson&Johnson, Netflix, Procter & Gamble, IBM, Tesla, and Verizon, who report today, Monday, October 18, or on Tuesday, October 19.

Is S&P 500 set for the previous top?

Last week was also a lovely week from a technical perspective. S&P 500 managed to retake both MA20 and MA50. Note also how MACD recently generated a weak buy signal. Will the current sentiment be enough for the previous top to be tested? On the way up, resistance can be found around 4 475:

S&P 500 Index graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart below, one can see how the index closed above EMA9

S&P 500, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Nasdaq got stuck

Nasdaq also went into the weekend on a positive note. However, as shown in the chart below, the index did not manage to break up above MA50. But as for S&P 500, MACD has recently generated a weak buy signal:

Nasdaq 100 graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

Nasdaq closed just above EMA9 with little margin in the weekly graph:

Nasdaq 100, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Amazon

One of the great FAANG-companies, Amazon, outperformed on Friday 15 October to close above Fibonacci 50 and marginally above MA100. MACD has generated a weak buying signal. The question is if buy-interest will continue to drive the stock upwards to the next level, around 3 500 USD?

Amazon share price graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

With the pessimistic glasses on, one can see a scary head-and-shoulders formation in the weekly graph. The formation signal carefulness if the share loses momentum during this week:

Amazon, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

The dominance of cyclical and value stocks in DAX

Germany and Sweden have high net exports to the rest of the world. The difference is that Germany is a larger market. Several other large countries with relatively high GDPs, such as France, Italy, and Spain, are situated pretty close to Germany. Hence, German companies have a high share of sales in continental Europe (often just under 50 per cent), with the rest going to other parts of the world, not least to East Asia with China in the lead. On the other hand, Sweden is a small country, so the large companies typically sell 90-95 per cent of their goods and services to the rest of the world, with perhaps no more than 25-35 per cent going to the rest of Europe.

With a small currency (SEK), Swedish companies are more sensitive to currency fluctuations, mainly against the euro and the US dollar. At the same time, the sizeable Swedish engineering companies have moved a large part of their production to the regions where end-users are found (Europe, North America, and Asia in the first place). But in these regions, the display is often located in low-cost countries such as Eastern Europe, Mexico, and China. German industrial companies have a significant advantage in relocating low-cost production to neighbouring countries like Poland, the Czech Republic, Slovakia, and Hungary. The low-cost production strategy also applies to US industrial companies, with factories in Mexico.

The largest company in the DAX index is the business system giant SAP. The second to sixth-largest companies are five industrials (Linde, Volkswagen, Siemens, Airbus, and Daimler), which account for 33 per cent of the total DAX index market capitalization. Next we find Deutsche Telekom followed by a blend of technology, banking, healthcare, consumer goods, and property companies. The DAX index comprises 40 companies, with the 20 largest accounting for 86 per cent of the total market capitalization.

The 15 largest companies in the DAX ranked by market capitalization

Source: Refinitiv Eikon

Nice move in DAX, but now at strong resistance

Cyclically oriented DAX rose by 2.5 per cent last week. In the daily chart, EMA9 and MA20 were retaken, and the falling trendline was broken. That is clearly positive, and MACD has generated a weak buy signal. But as can also be seen, the index now faces strong resistance close to 15 600, where MA50 and MA100 converge. Is there more energy left to take out this level?

DAX index graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

Resistance is also the case when looking at the weekly chart, this time in the shape of MA20:

DAX, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

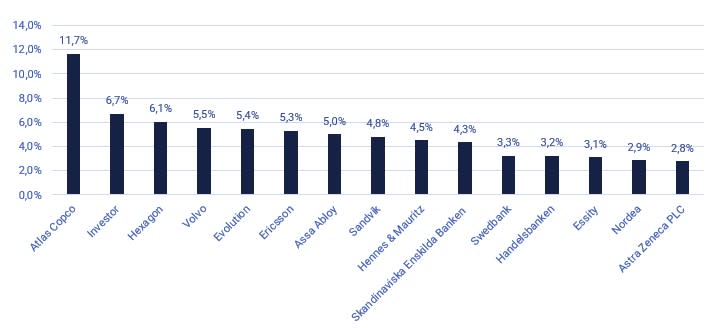

OMXS30, for value investors

Large engineering companies account for 43% weigh of the OMX30. (Note that weights for OMXS30 are based on turnover) To that, you could add four significant banks with 14% weight in the index. The OMX30 is, therefore, to a large extent, an index of cyclical and so-called value stocks. At the same time, the significant dependence on exports and currency sensitivity explains why OMX sometimes behaves like an emerging marketplace.

The 15 companies with highest weight in OMX30 account for 74% of the total weight.

The 15 largest companies in the OMX30 ranked by market weigh (turnover)

Source: Nasdaq OMX.

OMXS30 testing MA100

OMX30 rose by 3.3 per cent last week and is now testing MA100. MACD has generated a weak buy signal. Just above MA100 comes MA50. As for the other indices, the start of this weeks trading will be important.

OMXS30 index graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, OMXS30 bounced nicely of support. EMA9 was also retaken, but as for many of the indices, MACD is not supporting the upwards movement:

OMXS30, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Boliden is gaining from rising copper

Boliden is flying, and many thanks go out to the rise in copper prices. As shown in the chart below, the stock is now testing the falling trendline. Note how MACD recently generated a buy signal:

Boliden share price graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, the Boliden stock closed well above MA20 and MA50. Again the falling trendline is serving as a resistance:

Boliden, weekly five-year share price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Copper is flying

Copper has flown out of the falling trend channel. Can the previous top be taken out?

Copper price graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

Copper, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Weaker USD gives support to copper

Maybe the answer lies in the development of the USD. A weaker USD is good news for copper, and it is interesting to see the strong movement even though the USD has been trading in an unfavourable direction.

Below is EUR/USD. EMA9 is again on the rise, and MACD has generated a weak buy signal. A break of MA20 for the currency pair would definitely be good for copper, but also Boliden.

EUR/USD graph, March 12 to October 15, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly graph, the currency pair is supported by MA200:

EUR/USD, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Full name for abbreviations used in previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risici

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.