Is Europe losing the devaluation contest? Keep an eye on VIX

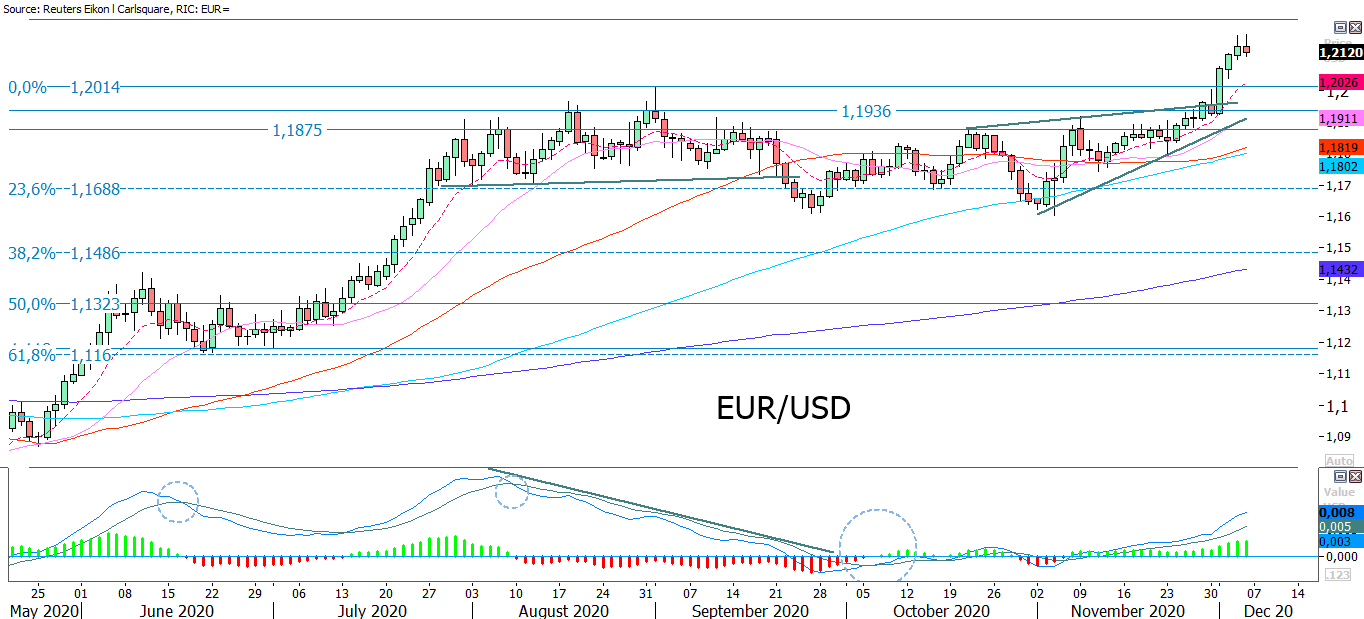

The Euro is now starting to test levels above 1.2 against the USD, which the ECB previously said is a critical point for them. There is now a great deal of debate about whether the ECB should intervene in any way against this strengthening of the Euro, which in the longer run will weaken Europe’s competitiveness against the rest of the world.

The Euro is now starting to test levels above 1.2 against the USD, which the ECB previously said is a critical point for them. There is now a great deal of debate about whether the ECB should intervene in any way against this strengthening of the Euro, which in the longer run will weaken Europe’s competitiveness against the rest of the world.

The main argument for the ECB to do nothing is that it is not the Euro that is strengthening, but the USD that is weakened by all the support packages cooked up by the Fed and incoming president Biden.

The big question that is being raised is whether the rising EUR/USD signals that the ECB has run out of ammunition. If the ECB and the EU cannot maintain the same rate of support as the US, the USD will continue to devalue against the Euro. Europe will then have lower growth than the United States. This is both since Europe launches lower support, but also because Europe suffers from a more expensive Euro. The absurdity of this context is, of course, that Europe is at the same time suffering from the self-imposed hostage Brexit, which is further weakening the continent’s economy.

The implications and arguments are many. The easiest thing is to try to ignore the noise and not to be over-smart. The currencies will show the way. The correlation is high between the USD and the stock markets: A rising USD gives a falling stock market, and vice versa.

Also note that interest rates are soaring in the US. This may show that the market is pricing in a rapid recovery next year. Rising interest rates are also a signal that many are selling US bonds. Our own view is that rising interest rates are a positive sign of a healthier economy. The market can probably live with somewhat higher interest rates. However typically the stock market disapproves rapid interest rate shifts, so this can create a downward pressure on stock markets if interest rates do not stabilize quickly.

We have long said that the US presidential election and the season speak for a strong end for the stock market this year. But the beginning of December can be tumultuous. There are signs that should be put in the spotlight because it can create a quick downward turn. Typically, however, we would see setbacks as a buying opportunity.

The graph below shows the S&P 500 index. Note how all shorter moving averages are trending upwards, but also that the index struggles with the rising trend line. Since the MA-lines are nicely arranged and trading upwards, the first interpretation is as stated, that a decline creates buying opportunities. We still believe in Santa Claus (although some say he should stay home since he belongs to the risk groups for Corona).

Tech-heavy Nasdaq has caught up on the broader S&P 500 index and set in a similar manner a new all-time-high on Friday, December 4th:

If we look at the options market, the excessive complacency among investors is shown. Below shows the Call-Put-Ratio which illustrates the ratio of issued call options and put options. This is a contrarian instrument, i.e. you follow it to see when it reaches extremes to go against the current trend. Right now, it is much more interesting with call options than put options. This shows that the options market is unusually positive.

The VIX index below, which show the market’s pricing of expected volatility over the next 30 days, is also at low levels. It usually pays off to buy protection when VIX reaches the lower Bollinger Band, which was very close last Friday.

A falling USD is putting upward pressure on commodities. When more and more investors discount for a recovery in the economy next year, raw materials will be hot.

First out is little Bitcoin which has made a real recovery and is currently trading close to the previous top:

The copper price has also broken up and is leading the whole raw material group. Copper follows the upper Bolling Band upwards. One of the first signal of lost momentum is when the rising EMA9 start to fade and MACD histogram begins to fall:

In the weekly chart, Brent oil is getting closer to Fibonacci 61.8. Note however that a somewhat scary doji was created in the daily graph below. The oil price is however still supported by a rising EMA9. In case of a break to the downside, the next level can be found around 46.75 USD/barrel followed by MA20:

The positive sentiment on the equity market has put pressure on the gold price, but the weaker USD added some fuel to the metal last week. As shown in the daily graph below, the gold price is currently testing both Fibonacci 38.2 and MA20. Note how MACD has generated a buy signal. In case of break to the upside, MA50 around 1 879 USD per troy ounce is the next level.

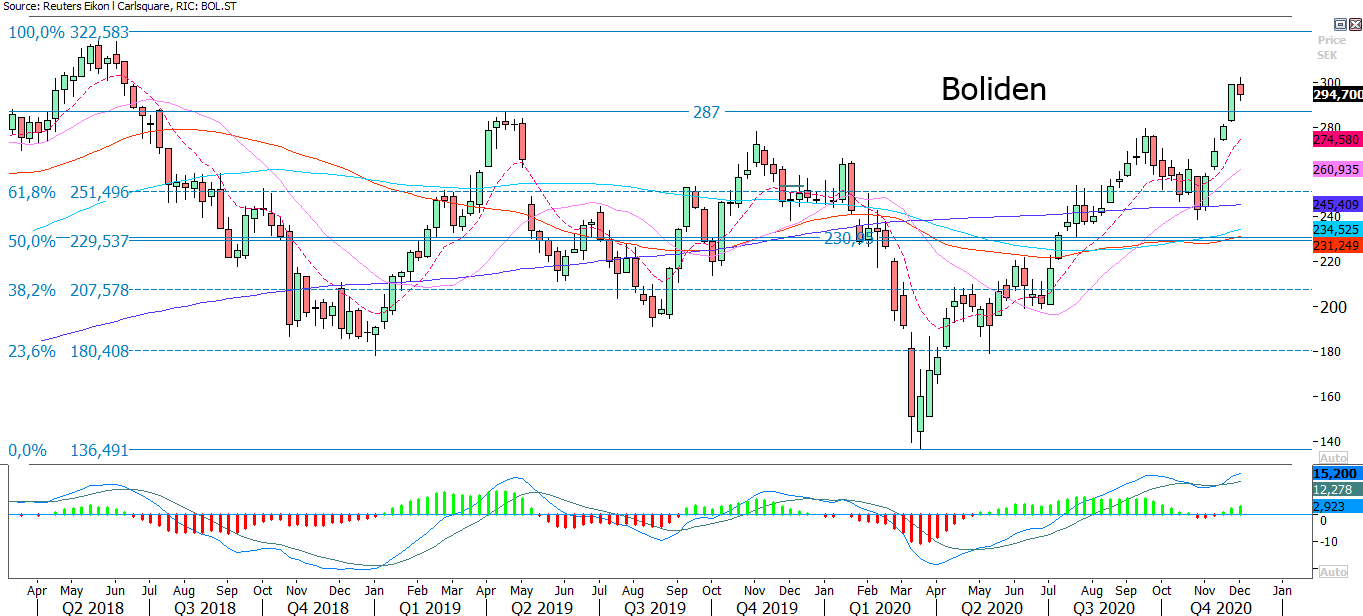

The Swedish Boliden stock has outperformed the Swedish index OMXS30 index. As shown in the weekly graph below, Boliden is getting closer to the previous local top from 2018. The question is now if this level ca be reached:

The OMXS30 index, on the other hand, is currently struggling with staying above MA20 and a previous top from February. Also note how MACD has generated a weak sell signal. In case of a break below the 1 905-level, the next level can be found around 1 880 followed by 1 855:

German DAX index seem never to be able to take out the gap from February. The index is losing momentum, which can be seen from the falling MACD-histogram. MA20 still serves as support. In case of a break to the downside, the psychologically important 13 000-level may come into play:

Risici

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.