Growth stocks highly valued prior to FANG reports

Last week was relatively uneventful from the perspective of the major indices. They are simply catching their breath and the market is waiting for a new push. Up or down?

Last week was relatively uneventful from the perspective of the major indices. They are simply catching their breath and the market is waiting for a new push. Up or down?

Challenging to say, but the fact that many Democrats must admit that Trump won the latest debate with Biden increased his chances of reducing Biden’s lead in the presidential election. As we have said many times: No matter who wins, there are great chances of a rise in the stock market. The downside is that the election is even and that the losing side appeals the election result. This risk naturally increases if Trump starts to rise in public opinion.

The S&P 500 index fell at the beginning of last week when President Trump and the Congress represented by House Speaker Nancy Pelosi appeared to have difficulty agreeing on a new stimulus package. Towards the end of the week, there was a recovery on the New York Stock Exchange backed by continued strong company reports, but also that the stock market concluded that there will be an incentive package, after the presidential election on November 3. Last week (October 19-23), the S&P 500 index fell by 0.5 percent.

On Tuesday 27 October, the index fell below MA50. Now, MA100 around 3 305 serves as magnet and support.

This week will be very intense with about 1/3 of the S&P 500 companies reporting their result for the third quarter. Among them we find many FANG companies such as Facebook, Alphabet (Google), Amazon and Apple that report tomorrow after closing in New York. Combined these four companies represent 16 percent of the S&P500 index value, so the outcome here is likely to be decisive for the continued stock market price development.

Amazon just opened their first site in Sweden that seems to be full of growing pains. Also, Amazon report their interim result tomorrow:

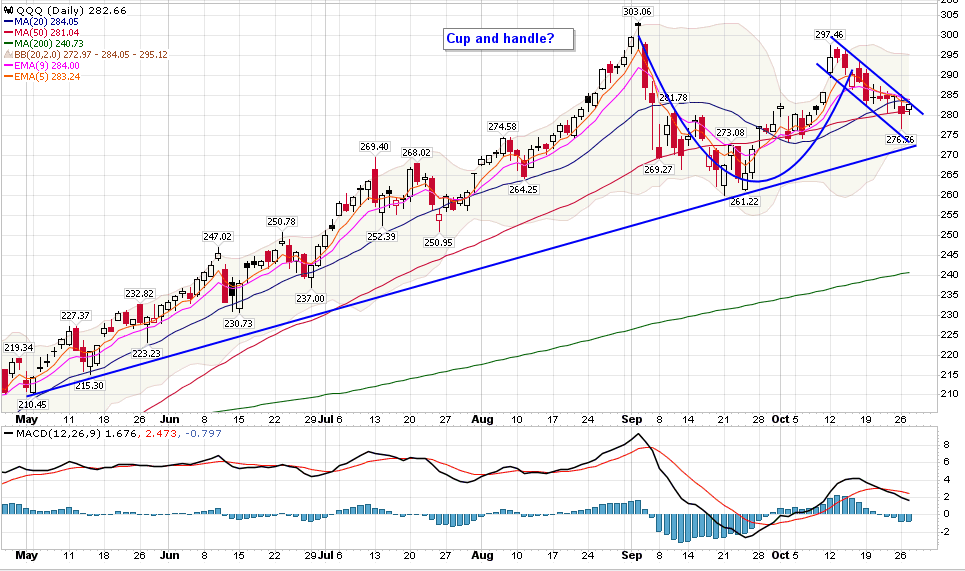

Tech-heavy Nasdaq index has formed an interesting cup- and handle formation. If Nasdaq falls out of the declining trend channel, it could create a new rising trend.

The strong company reports in the US also seem to have begun to affect the long-term interest rates (10-year US government bond) below, which has risen from about 0.6 to 0.76 percent so far in October. On the other hand, the ten-year US government bond was traded in the range of 1.75-1.9 percent interest rate as late as November-December 2019. There is a bit left to a normal mode.

The USD has strengthened against the Euro as markets gotten shaky in the wake of worries for another wave of restrictions due to increasing number of Covid-19 cases. As shown in the graph below, the currency pair EUR/USD is approaching a support around 1.17. The next level on the downside is made up by MA100 around 1.165:

Rising inflation favors value stocks

We have been writing a lot for several years about the leading role of FANG shares in the global price increase on the world stock exchanges. The chart below shows the fall in value stocks relative to the growth companies on the New York Stock Exchange. As can be seen, this is a good halving of the ratio between value and growth on the S&P index since 2007.

An economic explanation for this may be that the central banks, through their low interest rate and support policy, have killed inflation (for ordinary goods and services, but not for asset prices). Value stocks are performing best in an environment with a positive interest rate and a yield-curve, i.e. expectations of successively higher prices. This is not how it looks currently. The question is when such a change could materialize. Not within shortly if you ask us… even if we agree that the value differences have become remarkably large. That inflation is now rising again in the US is still positive for value shares, all other things being equal.

But it is not true that growth stocks (especially then FANG) would only rise on a macro trend. These companies’ shares also go up or down on actual report results. Digitalization is a significant factor in change in society. We only need to mention Amazon to realize that there is and has been a change that at least partially corresponds to these shifts in value. While production costs have been reduced, the value of brand and distribution power has increased exponentially. That differs from internet consultants and the like around the turn of the millennium. Then there are growth companies even today that have most left to prove, such as Tesla.

Then we have the valuation aspect. The value of profits well into the future (which typically growth companies have) increases in a low interest environment. We have illustrated the falling return requirement from a Swedish perspective in the graph below. The interest rate on a ten-year Swedish government bond has gone from 4.0 percent in February 2008 to around zero percent in May 2020. But investors´ market risk premium on the Stockholm Stock Exchange has increased from 4.9 per cent in 2008 to 7.7 per cent in 2020 according to PwC´s annual risk premium study. This reduces the justified increase in value (higher p/e ratio) to only 16 per cent between 2008 and 2020 from a Swedish investor perspective. We then disregard the market capitalization premium (which is approximately 1 per cent for larger companies on the Stockholm Stock Exchange), the beta ratio and company-specific risk supplements.

That the New York Stock Exchange is valued higher than what is fundamentally justified is something that ZeroHedge highlights in connection with the American investor icon, Jeremy Grantham, having taken a net short position vis-á-vis the stock market for his portfolio worth 5.7 billion USD. In an interview with CNBC, Grantham points out that the New York Stock Exchange has risen in a way that has no historical equivalent, at a time when the economy has suffered a downturn.

What is the conclusion of this? We follow the graphs to find the timing in the market. But the likelihood of reversal in investment sentiment has increased with rising US interest rates. One idea is to buy Swedish value stocks as a more defensive play. If the market goes down, these will of course also be included, but the decline should be smaller Furthermore value stocks have historically been stronger in a situation of rising interest rates.

We suggest two investment companies, Industivärden and Investor, as these, with two large equity portfolios, capture a large part of the industry, forestry, the telecom and banking sectors on the Stockholm Stock Exchange. Industrivärden and Investor were valued with 6 and 16 percent respectively, NAV discount as of 30 September 2020.

As the other three value shares in the value equity portfolio, we choose Handelsbanken, SCA and Volvo. Handelsbanken´s share has performed poorly for a long time, which has had its reasons. But banks are benefitting from rising interest rates. We have seen such an increased interest to buy US bank shares for this reason in recent weeks. SCA has large forest assets that provide a good hedge against excess price declines. Volvo finally submitted a strong Q3 report and has a record amount of liquidity, which increases the chance of a larger dividend to shareholders in the spring of 2021. In general, one should look for shares that can offer a high yield, which is usually a good hedge against major declines. These shares are now also bought by fixed income managers as an alternative to interest rates that provide almost no return at all.

The Volvo share gapped down below the rising trendline as well as MA50. The question is now whether the gap is to be closed or if this was a break away gap. The upcoming trading days will give more information on this.

OMXS30 is struggling and gapped down below MA100 but managed to trade back up above a support around 1 725. Again, more information on whether the gap shall be closed or if it is a break away gap will be given in the upcoming trading days. Note that MACD has generated a sell signal. The next level on the downside can be found at MA200 around 1 694:

German DAX index is leading the fall and is currently trading below its MA200. The next level on the downside can be found around 11 480 where Fibonacci 38.2 meet up:

Investors tougher on report failures

When approximately one third of the S&P500 companies have reported their results, the proportion of profit-positive surprises relative to the stock market´s forecast is 84 percent. Revenue surprises are at 81 percent with the Energy and Real Estate sectors at the lowest levels (50 and 33 percent respectively). It is noteworthy that the Industrial sector has worked its way up from 56 to 74 percent higher than anticipated revenues in one week. On the Stockholm Stock Exchange, it has otherwise been a theme lately, that positive profit surprises are not enough. Currently, a positive trend in revenue and order intake is also required- which would explain why Volvo´s Q3 report was received better than Atlas Copco´s.

But the S&P500 companies’ profits, are still 18 percent lower, while revenues have decreased by 3 percent in one year´s time. This is visualized in the graph below, where the fall in corporate profits corresponds to the dark blue line. The chart also shows how the gap between the S&P500’s P/E ratio and companies’ profits has increased significantly during the last two quarters.

Investor tougher on reports flops

Below is the table with earnings and revenue outcomes for the S&P500 companies for the third quarter from 10 September until 23 October.

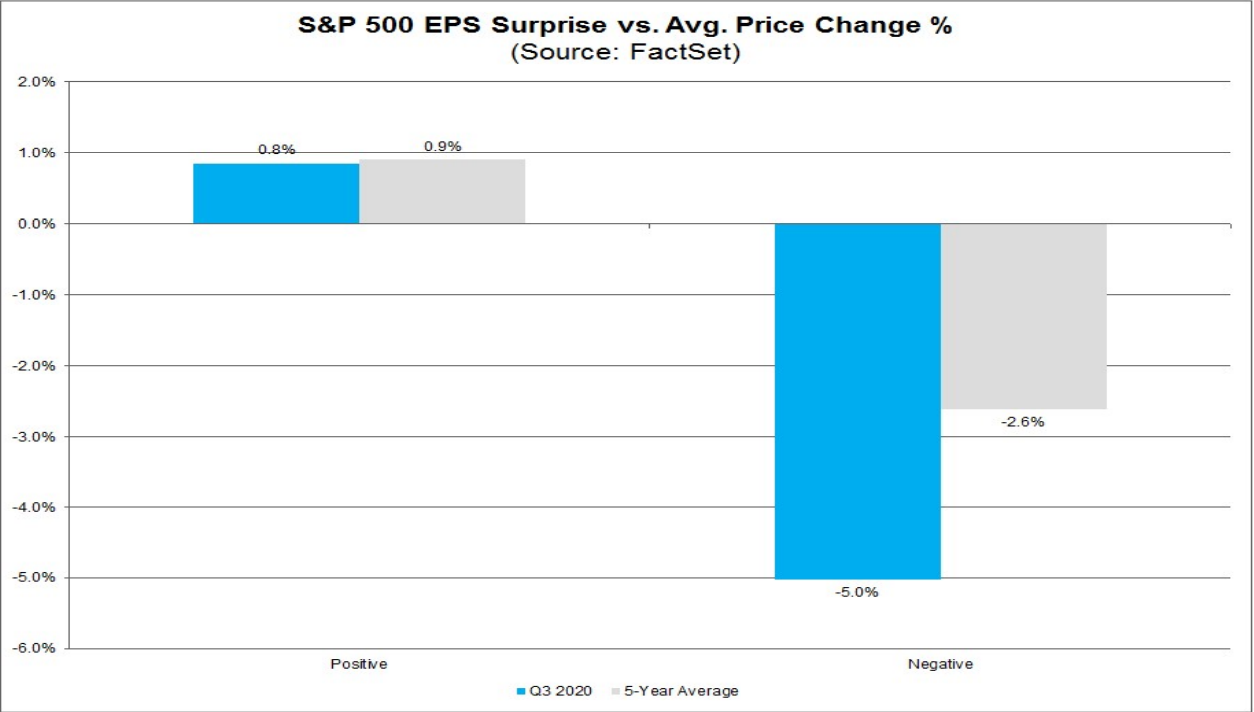

Share prices in positively surprising companies have risen in line with the earnings surprise during the reporting season for the third quarter. On the other hand, the market is a little less forgiving towards companies that deliver profit disappointments, as can be seen from the graph below. The price drop for such companies has been 5.0 percent so far during Q3 2020, compared with only minus 2.6 percent as an average over the past five years.

Source: Earnings Factset.

Bitcoin was last week’s winner and is still up during this week. However today, Bitcoin is falling with most other assets today. As shown in the weekly graph below, Bitcoin a trading right below a resistance made up by Fibonacci 61,8. In case of a break to the upside, the next level can be found around 16 230:

Risici

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.