Cow release in the UK opens for travel and leisure stocks

There is a cow release now in the United Kingdom with restaurants opening. The travel sectors can speed up with a high proportion of vaccinated UK citizens. It can make shares in hotels, air lines, restaurant chains, and retail interesting. Real estate stocks with focus on offices and retail have also lagged.

There is a cow release now in the United Kingdom with restaurants opening. The travel sectors can speed up with a high proportion of vaccinated UK citizens. It can make shares in hotels, air lines, restaurant chains, and retail interesting. Real estate stocks with focus on offices and retail have also lagged.

The pattern we see now in the United Kingdom is likely to be repeated a few months later in the rest of Europe. Swedish equities in the crisis sectors generally have a longer way to go to earlier price peaks than their British colleagues. The recovery game may therefore be more interesting to play on the Stockholm rather than the London Stock Exchange.

The UK, where many of the pharmaceutical companies are headquartered, has succeeded best in the developed part of the world in vaccinating their population. The vaccination league is led by the United Kingdom with 48 percent of its population, followed by the United States with 38 percent and the EU where on average only 18 percent has received a few doses.

On Monday 12 april, shops, hairdressers, gyms and outdoor cafes in the UK opened. The fact that the infection has decreased rapidly in the UK also contributed to these reliefs. The phenomenen can be compared to a cow release (see picture above). The cows are overjoyed to feel the warm spring winds and the grass under their feet again. Something similar is likely to apply to people who have been detained as a result of Covid-19 restrictions for over a year. Who doesn´t want to have a beer at an outdoor restaurant or go on that golf trip to Portugal that has already been postponed twice? Maybe you should go shopping for clothes in the middle of the week as well?

This article sums it up quite well:

The London Stock Exchange (FTSE 100) is trading past previous local highs from January and late March. Momentum is positive and increasing.

The FTSE Hotel and Leisure Index is rising but has not yet recovered the local top that was noted in March 2020, right before the break-out of the Covid-19 pandemic.

Swedish Scandic Hotels is behind the UK hotels in the business cycle. Capacity utilization was at a record-low of 23 percent in Q4 2020. This can be compared with some 40 percent during the Swedish financial crisis 1990-1994 and 66 percent for FY 2019. It feels more exciting to be on the ball early and play the hotel recovery game on the Stockholm Stock Exchange, rather than London, which is ahead in the chain of events. The vaccination is being carried out in Sweden as well, although delayed by some months.

One share in the travel sector that seem to have gone in for a gliding landing is SAS. The company raised SEK 4 billion in a new share issue in October 2020. The question is whether the money will last for the entire crisis. But the SAS stock has not yet risen that much and has a long way to go to the old top. Perhaps it would need a little aviation fuel…

Shares in office real estate companies have performed poorly since March 2020. Land Securities is one of the leading property companies in London. Offices have not been hit as hard as shops, hotels, and restaurants yet. But analysts in the sector point out that second-hand vacancies have been on the rise and that office rents will fall when vacancy rates surpass 7 percent.

One share that has fallen deeply without a tendency to recover is Hufvudstaden. The company owns a considerable part of the office and retail properties in Stockholm CBD. The company has had major challenges with NK department store, where the landlord (Hufvudstaden) had to take over the operations for one of its main tenants. But if there is any company that has financial staying power, it is Hufvudstaden with an LTV of only 20 percent.

Currency headwinds for the Swedish exporting companies in Q1 2021

This week, the Swedish Q1 2021 reporting season begins with Sandvik on Tuesday, Ericsson on Wednesday, and Volvo on Thursday. The expectations that the industry has performed strong during Q1 2021 are solid and mainly apply to operations in North America and Asia. However, closures in some major countries in Europe may have had a negative effect. The comparative figures are easy to surpass, especially in China, where the authorities made hard shutdowns in Q1 2020, while this effect did not become visible until March 2020 in Europe and North America. In these regions, Q2 2020 was the weakest. It is thus such an easy comparison that awaits the next reporting season for Q2 2021 in July and August.

As for the Swedish Engineering companies, they often have 80-95 percent of their operations outside Sweden. It is only Ericsson and Volvo and to some extent Sandvik that still have a relatively large net export from Swedish factories. But the effect of the stronger Swedish krona is still likely to have a significant effect through currency translations on the operations of the foreign subsidiaries. In the graph below, we show how the EUR/SEK and USD/SEK exchange rates have changed since Q1 2019 (which is compared with Q1 2018). As can be seen, the positive conversion figures have turned into negative ones from Q3 2020, and the effect has increased up to Q1 2021.

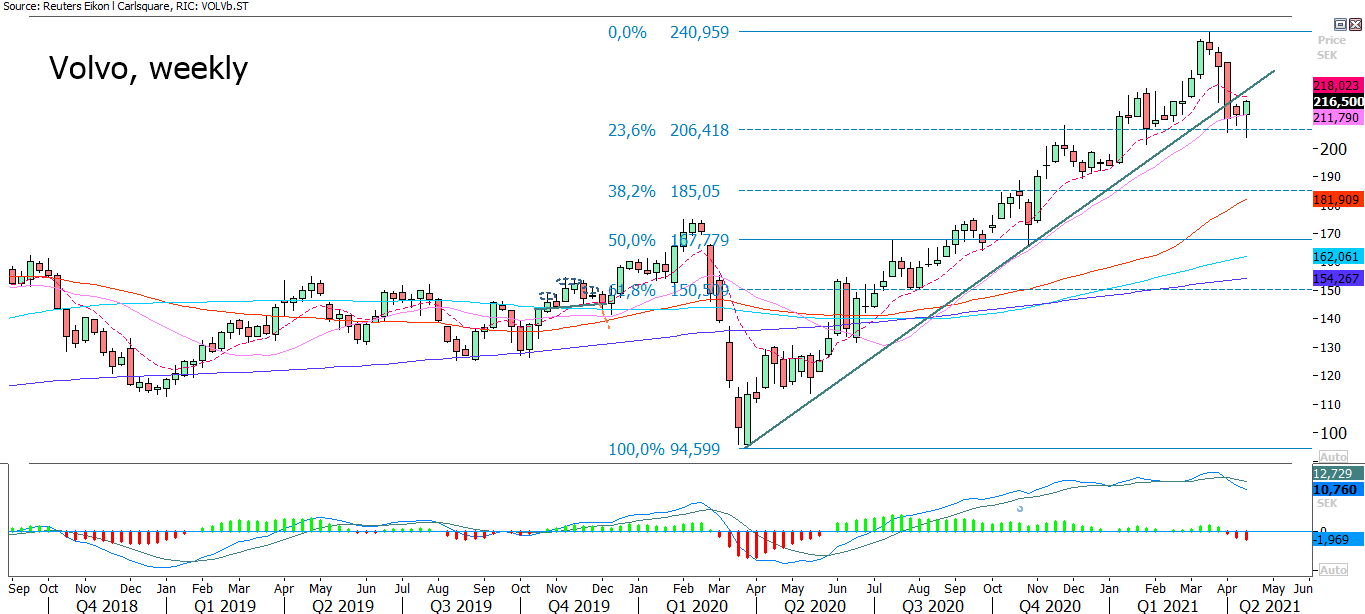

Below is the Volvo share. The company has already been communicating that lack of semiconductors has led to trouble in the production chain. The share has also been under pressure. What will the report say about the future?

After the past week 44 out of 503 S&P500-companies or about 9 percent of all have reported their Q1 2021 revenue and earnings figures. As can be seen industrial and various types of consumer goods companies have had a relative challenging time to surprise on a positive note. Overall, the earnings outcome is very strong so far with 84 percent of the results better than anticipated. Companies that have disappointed the stock market are e.g., Carnival, Costco Wholesale, Delta Airlines and General Mills. We are talking about cruising companies, retail, airlines, and food manufacturing companies- i.e., sectors that has been hit by the Covid-19 restrictions.

Momentum

US interest rates are starting to fall back to the level where the Fed is said to want them to be. It is probably more of a speculation than facts, but possibly the concern about the high interest rates is over for this time. Alternatively, it will pick up with renewed momentum by 1.5 percent for the 10-year US government bond as support.

Falling rates have contributed to pushing tech heavy Nasdaq above its previous top. Note the scary doji that was created on Friday 16 April:

The Tesla share is having trouble breaking through the resistance:

EUR/USD has stuck to MA50 as well as Fibonacci 50, just below the critical level for the ECB:

The DAX index breaks out after a phase of consolidation:

OMXS30 index had a similar move on Friday 16 April:

Keep track on the Shanghai Stock Exchange. China tends to be ahead of the Western world. SSEC slides on MA200. Should it form a basis for an upturn, or will the index break down? It is likely to be telling for the entire global stock market what direction that is being taken.

The gold price breaks up above MA50 after a double bottom. Fibonacci 38.2 is the next level:

Risici

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.